The independent Irish Financial Services Appeals Tribunal (the Tribunal) has recently published a judgment (the Judgment) in relation to a decision by the Central Bank to refuse an individual's application to a pre-approval controlled function (PCF) role under the Central Bank's fitness and probity (F&P) regime.

The Judgment in the case of AB -v- the Central Bank of Ireland found that the Central Bank's decision-making process was flawed, with the Appellant being denied fair procedure at each stage of the process. As a result, the Tribunal determined that the Central Bank's decision was legally "incorrect" and has returned the application to the Central Bank for reassessment with directions for future steps to be taken.

Review of the Fitness and Probity regime

The core function of the statutory F&P regime, introduced in 2011 is to ensure that individuals in key decision-making and customer-facing positions in a regulated firm are competent, capable, honest, ethical, of integrity and financially sound.

Based on the evidence of one Central Bank Official, Mr Des Ritchie, in 2022, there were as many as 3,500 PCF applications. Of these, some 3,000 were approved quite speedily. The Central Bank's service standard is that 85% of such applications should be approved within 12-15 days - around 98% of applications were dealt with within that time span, with the remaining 2% to 3% being subject to further scrutiny.

Background

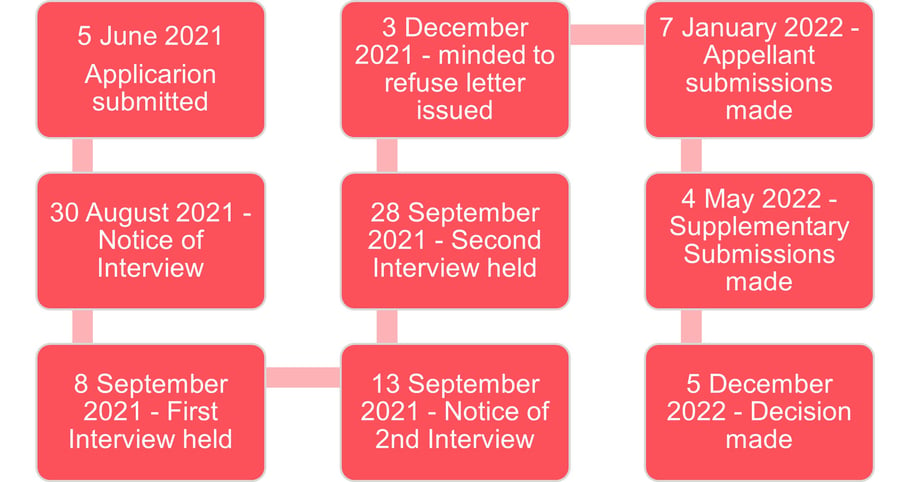

Applications had been made on the Appellant's behalf in 2020 for approval of a number of PCF positions but the Central Bank made no decisions on these. A further PCF application was made on behalf of the Appellant in June 2021.

The Central Bank's approval procedure followed the following steps:

1. the Appellant was first called in for an "assessment interview";

2. a "specific interview" followed and these both made adverse findings;

3. a "minded to refuse" letter confirmed these adverse findings;

4. submissions was invited and ultimately delivered by the Appellant within the timeline; and

5. the applications were refused.

The timeline for the application showed lengthy delays in the process which were largely unexplained:

On 5 December 2022, the Central Bank issued a decision (the Decision) that, under the Central Bank's F&P Code, the Appellant was unfit to hold the two positions of (a) Non-Executive Director (NED) - PCF2 - and (b) Chairman - PCF3 - of a UCITS ICAV authorised by the Central Bank.

The Decision included reference to matters which occurred in 2019, when the Appellant had been involved in an AIF and a number of bond investments which the AIF made became seriously impaired.

At the time of the Appellant's application which led to the impugned decision, he was approved by the Central Bank to act as a NED or Chairman of seventeen regulated entities in this State, and one regulated fund administration company.

The Appellant appealed the Decision to the Tribunal. The appeal hearing itself was heard over 4 days and the Tribunal had to consider some 1,500 documents. The case was fought on an adversarial basis.

The Tribunal concluded that the Central Bank's decision-making process was flawed and that the Appellant was denied fair procedures at each stage of the process.

The Judgment makes a number of directions concerning future steps.

What did the IFSAT conclude?

(a) The assessment interview

The Tribunal found that, in relation to the assessment interview, it is "abundantly clear" that the Central Bank fell below the standards of fair procedures which should apply to ensure an applicant (here, the Appellant) has fair notice of the issues to be covered at the interview - the interview was the first step in an important regulatory process, which impacted the Appellant's right to earn a living.

In particular:-

while the Appellant was informed that he was to be examined regarding his knowledge of the regulatory environment, some of the questions he was asked were "unnecessarily granular" and "sometimes unclear". It was clear that the decision makers had 'matters on their mind' which were not set out in the invitation, and should have been; and

a person being interviewed is entitled to be questioned fairly - some of the questions put to the Appellant were "extraordinarily complex", with many sub-clauses.

As a result, the Tribunal concluded that, at the assessment interview, "there was an absence of fair notice sufficient to conclude that this part of the process fell below the standard of constitutional fairness".

(b) The Specific Interview

The Tribunal determined that many of the above criticisms could also be made in respect of the specific interview. It also observed that while there was the appearance of fair procedure, there was an absence of its substance

The flaws from the Assessment interview fed into and were reflected in this interview.

The invitation to the specific interview was broad and unspecific in its terms,

The Appellant was not given full notice of the issues which were going to be explored.

Some of the questions were exceedingly granular and detailed and would require considerable expertise.

The Appellant was not given full or fair notice of the issues which were intended to be explored.

The absence of notice regarding the white folder circulated to the Appellant the day before the specific interview was also criticised.

The Central Bank official who carried out the main questioning at the assessment interview and played a major role in the specific interview had been involved in an earlier investigation, in which the management of a firm of which the Appellant had been Chairman was seriously criticised.

(c) The CBI Decision

Although the official who made the decision to issue the impugned decision (the Decision Maker) had not been directly involved in the interview process, she was reliant on the information which emerged from a previously flawed interview process and reached conclusions on the inadequacy of the Appellant's answers.

These, though, were in response to questions posed where the Appellant had not been given fair notice of the issues to be raised.

Although the Appellant submitted a significant amount of material which set out "a point-by-point critique and rebuttal of the interview process as a whole" and challenged the fairness of the procedure, the Tribunal found that the Decision Maker failed to give this fair consideration but, instead, focused unduly on the Appellant's knowledge of the regulations and his performance at the two interviews.

The absence of a determination in relation to the significant, countervailing and rebuttal evidence was viewed by the Tribunal as more significant in light of the fact that there was, for that reason, a failure on the part of the decision-maker to give reasons for her decision,

(d) The Tribunal's findings

The Tribunal concluded that the CBI fell into errors of law, which were such as to vitiate the conclusion reached. There were, then, fundamental procedural flaws at all three stages of the process and the Tribunal was satisfied that the Central Bank's procedure did not comply with the need for fair notice, the duty to give reasons and observing the principle of hearing the other side.

The matter is remitted to the Central Bank for reconsideration, under the following directions:

the Central Bank must notify the Appellant, within 21 days of the Tribunal's decision, of the procedures it will apply in reconsidering the applications

the process is to be carried out by persons who were not directly involved with the matters considered in this decision.

the reassessment process must be completed within 90 days of the date of issue of this decision.

Central Bank Statement in response to the Judgment

Following the publication of the Judgment, the Central Bank confirmed that it will immediately conduct a reassessment of the application in accordance with the Tribunal's directions.

The Central Bank has also confirmed that since the F&P approval process is now more than a decade old, it has decided to commission an independent review to ensure that it remains effective for the future - the outcome of the review will be published in due course.

Meanwhile, all of the Central Bank's gatekeeping functions, including the F&P approval process, will continue to operate in accordance with agreed service standards.

_11zon.jpg?crop=300,495&format=webply&auto=webp)

_11zon.jpg?crop=300,495&format=webply&auto=webp)

_11zon.jpg?crop=300,495&format=webply&auto=webp)

.jpg?crop=300,495&format=webply&auto=webp)