The future of the European NPL-Market

An overview of recent market trends and drivers for NPLs.

What are NPLs?

Our Insight deals with the European NPL-Market. In very simple terms, NPLs are non-performing-loans, i.e. credit obligations, usually owed to a bank or other credit-institution, which are or will likely become “payment-impaired”. There is no universally accepted definition of non-performing-loans. However, the standard definition (used, inter alios, by the European Central Bank (ECB)1, the European Banking Authority (EBA)2 and the German BaFin3) refers to the following conditions:4

Overdue >90days. A loan that is overdue (due but unpaid) for more than 90 days. According to the EBA guidelines5 which are followed inter alios by the BaFin6, statutory deferrals are not included within the 90 days period. This preference includes, for instance, statutory COVID-19 deferral schemes or deferrals based on court orders (e.g. to safeguard a restructuring plan within a pre-insolvency rescue proceeding).

UTP-Event. UTP means “unlikely-to-pay”. Each bank has its own set of internal rules and guidelines relating to UTP-Events; some events can be seen as indicators, such as the insolvency of the debtor or another member of the debtor’s group, (continuing) breaches of financial covenants, failure to refinance or severe disruptions of a debtor’s supply chain (e.g. the insolvency of a main supplier).

Large NPL-Volumes have been a significant risk to the stability of the financial system in the aftermath of the world financial crisis and have led legislators all over the world to set up legal rules and guidelines to prevent NPL-Volumes from rising too quickly.

The current state of the European NPL-Market

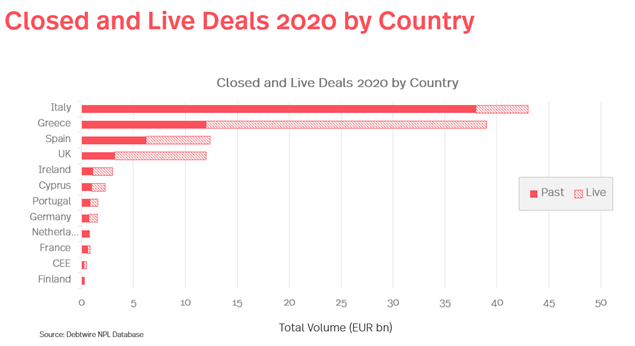

With the exception of some Member States, non-performing-loans on bank balance-sheets were generally under control. In the last years, NPL-Volumes were in fact in decline and financial regulators all over Europe have kept a watchful eye on any negative developments. In addition, countries with high NPL-Volumes like Italy or Greece have set-up successful securitisation schemes to manage systemic risks (see below).

At the beginning of the COVID-Crisis in March 2020 there was the expectation that insolvency filing rates and – as a consequence – NPL-Volumes would instantly rise. At least for 2020 and 2021, quite the opposite was true. Insolvency filing rates in most Member States went down and, for instance in Germany, hit rock-bottom at the height of the crisis in September 2020.

State-Aid-Programmes and insolvency moratoria have prevented a melt-down. By mid-December 2021 the German government has provided more than EUR 129.4bn7 in the form of direct or indirect subsidies to the economy, strikingly referred to by German chancellor Olaf Scholz in his role as the German finance minister (as he then was) as a “cash-bazooka”. In addition, the ECB has used its PEPP-Programme8 to buy governmental bonds on a large scale and keep the markets liquid.

Since the last quarter of 2021 we are experiencing a moderate increase in insolvency filings in Germany.

.jpg)

The German insolvency moratorium has terminated at the end of April 2021. Insolvent debtors are once again under a strict filing-obligation in case of illiquidity and over-indebtedness. In addition, inflation of commodity and energy prices as well as supply-chain disruptions caused by the semi-conductor shortage have put significant pressure on automotive suppliers and enterprises in energy-intense sectors as well as electricity trading houses.

“Zombies” and other drivers for NPLs

The NPL-Market in Europe has been set into hibernation during the COVID-Crisis, but it is now slowly waking up again. In a recent survey, 90% of banking professionals have told Ernst & Young that they expect rising NPL-Volumes in the near future.9 Moreover, a study from the German NPL-Association (BKS) is predicting a 46% increase of NPLs in Germany in 2022 compared with 2020.10

In our view, the “waking-up-process” will be further stimulated by three factors:

End of State-Aid-Programmes. These won’t go on forever. For instance in Germany, access to short-time-work-schemes has been extended until the end of the first quarter of 2022.11 Once these programmes have eventually dried-out, unprofitable and over-indebted firms will come under pressure and it is to be expected that some will lose their investor’s confidence. It should also be noted that banks will be forced to comply with the required liquidity coverage ratios after the ECB no longer sees the need to extend the COVID related relief measure, which allowed inter alia banks to operate with liquidity coverage ratios below 100%, beyond December 2021.12

“Zombie-Lending”. During the COVID-Crisis governments all across Europe have induced banks to engage in what is referred to as “Zombie-Lending”13, i.e. lending and forbearance measures granted to firms which would have otherwise been taken off the market. “Zombie-Firms” have tripled since the financial crisis and have risen by more than 13% in 2020 alone.14 “Zombies” are particularly fragile and may not be able to adapt to post-COVID stressors in the absence of further state-subsidies. “Zombie-loans” therefore have the potential to significantly drive NPL-Volumes in the aftermath of the COVID-Crisis.

“Tapering” of Monetary Policy. Rising inflation throughout Europe and the U.S. is seen by many as a direct effect of an ultra-lax monetary policy.15 The U.S. Federal Reserve has reacted and will rapidly step out of quantitative-easing measures like buying government bonds. It has also declared to raise interest rates from the second quarter of 2022.16 The Bank of England has very recently raised its interest to 0.25%.17 The ECB has declared to terminate its PEPP-Programme until the end of the first quarter of 2022.18 Nonetheless, should inflation not be brought under control very soon, rising interest rates and a further “tapering” of monetary policy are the only measures that will be left for the ECB. Rising interest rates, however, will probably correlate with increased insolvency filing-rates, as debtors will breach their financial covenants in floating-rate loans and debt-refinancings will become more burdensome and costly.

The European Action Plan

Preventing systemically-critical NPL-Volumes has and remains a key priority for the European Union. The Commission has issued an Action Plan on preventing NPLs in December 2020.19 It is to be expected that the EU will increase the pressure on banks to proactively reduce NPL-Volumes.

We believe that the following elements within the EU’s NPL agenda may play a role in “resurrecting” the NPL-Market across Europe:

- NPL-Backstop. This was introduced in the EU in 2019.20 Once an NPL has been identified as such by an EU credit-institution, it must be backed with core-equity after a certain time has lapsed. For example, unsecured NPLs must be backed with 100% of core-equity after three years; for secured NPLs core-equity-backing starts after 3 years with 25% and then gradually increases to 100% after 7 years. In addition, the ECB’s guidelines (applicable to systemically-relevant credit-institutions) are even stricter and, for instance, require unsecured NPLs to be adequately backed with 100% of core-equity already after 2 years.21 The first significant “backstops” may come into play as early as 2022.

Market Regulation. The EU wants to regulate the NPL-Market to make it more efficient. The aim is to significantly reduce the bid-ask-spread which is still one of the major limiting factors for NPL trading. The EU’s regulatory initiative covers the establishment of an EU-wide Data-Hub (similar to the European Data Warehouse) where standardised information on historic trades will be available.22 The EU has also adopted a directive on credit purchasers and servicers, likely transposed during 2023, which allows for cross-border “passporting” of NPL purchasers and servicers.23 The EU also actively promotes the standardisation of private transaction platforms (e.g. DebtX, Debitos) which are supposed to function as a common marketplace for NPL trades.24

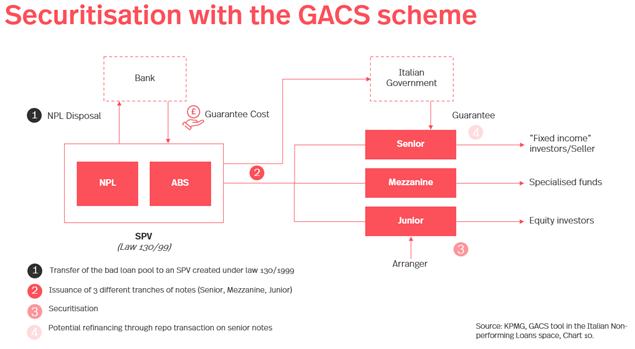

Securitisation. NPL securitisation has not really been used much in the aftermath of the world financial crisis. With two prominent exceptions, Italy and Greece with their statutory schemes GACS and HAPS. An SPV is used to acquire a loan-portfolio from a bank and refinances the acquisition by issuing tranches of senior, junior and mezzanine notes. The senior notes can be guaranteed by the state. The EU has given its blessing and has amended the EU Securitisation Regulation in March 2021 to facilitate NPL securitisations in all Member States.25

- Asset Management Companies. The EU supports Member States to set-up Asset Management Companies (AMCs), also known as “Bad Banks”.26 Examples for AMCs are the Italian AMCO, the Spanish SAREB, the Irish NAMA or the German EAA and FMS.27 The legal nature of AMCs can vary significantly among Member States. Some are public agencies (EAA) whereas others are private companies (AMCO). Some were founded with a single purpose, for example the EAA to acquire the NPL-Portfolio from German state-bank WestLB. Others are regular “players” in their domestic NPL-Market (AMCO). The ECB has recently suggested to set-up an EU AMC which could operate in all domestic markets.28 There has not been any feedback on this proposal from the Member States, so it needs to be seen if it will be taken further.

Managing NPL-Risks

In line with the majority market position, we assume that NPL-Volumes will rise in the near-future. However, lenders still appear to be in “wait-and-see-mode”, whereas we think they should switch to “action-mode” sooner than later. As a precautionary measure, lenders should set-up internal processes to effectively identify and manage potential NPL-Risks.

If NPLs are identified early, lenders will essentially have the following options:

Workout. The NPL is handed-over to the lender’s “intensive-care-unit”. This unit needs to be structurally independent from the loan-team responsible for the original financing decision.29 In such case, NPLs remain on the bank’s balance sheet and become subject to the NPL-Backstop. Typically workouts include stabilisation measures such as standstills, deferrals or prolongations to allow for enough time to prepare a restructuring proposal. The actual proposal can include various measures, such as haircuts, debt-equity-swaps, rescue-loans or novations into PIK-loans. Restructurings can also include the use of “hybrid” proceedings, e.g. an a German StaRUG or a Dutch WHOA.

Outsourcing. A bank can hire a professional loan servicer who manages the portfolio for the bank. This may be an option in particular for larger portfolios of NPLs. In contrast, a workout may be used where a lender has a large exposure to an individual debtor. Outsourcing is subject to important regulatory limitations, e.g. in the case of full or partial outsourcing of the special functions of risk controlling function, compliance function and internal audit.30 Like workouts, the NPL will remain on the bank’s balance sheet and will become subject to the NPL-Backstop.

True-Sale. A transfer of the NPL to a new investor, often a debt-fund or an AMC. True-Sales either include full transfers of legal title by way of asset deals or - somewhat rarer - de-mergers. The NPL will be taken off the bank’s balance sheet and will no longer be subject to the NPL-Backstop.

Synthetic Risk-Transfer. All or part of the economic risk is transferred by way of a funded or unfunded sub-participation, trust agreement or derivative instruments like credit-default-swaps. The lender will remain as lender-of-record but will be partly or fully indemnified by the investor. If the risk transfer is funded, usually all of the risk and opportunities will be transferred and the new investor will pay for the transfer. Synthetic Risk-Transfers are also used as an intermediate step towards an outright transfer of the full legal title. Once all consents are received or other requirements are met, the Risk-Transfer is “elevated” to a full transfer and a remaining price or premium may be paid. As the new investor has to bear the insolvency-risk of the lender of record, at least as long as the transfer has not been “elevated”, some Member States (e.g. Germany) allow the new investor to be registered in the lender of record’s refinancing register.

Securitisation. NPLs are transferred to an SPV which refinances the sale by the issuance of different tranches of notes. In case of the Italian GACS or Greek HAPS the senior notes are state-guaranteed. The NPLs are usually managed by an AMC on behalf of the SPV. Synthetic securitisation structures are also possible by which only the economic risk in the NPL is transferred to the SPV. The EU has facilitated synthetic NPL securitisations by amendment to the EU Securitisation Regulation31 and the Capital Requirements Regulation32 in March 2021.

The Buy-Side: Increasing Dry-Powder

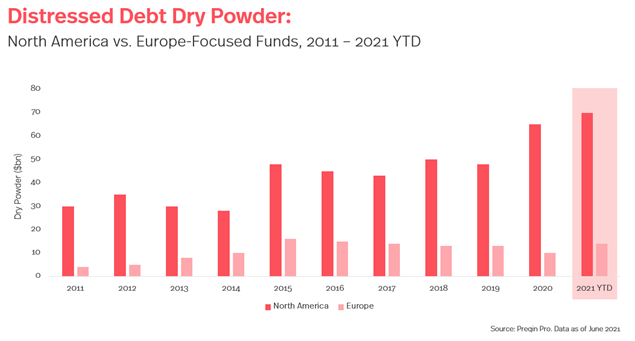

Fiscal policy, State-Aid-Programmes and other support measures have kept credit-defaults at an historically low level during the COVID-Crisis. For distressed funds, there was not really much to invest in the past months. Unsurprisingly, EU orientated funds have accumulated significant amounts of dry-powder during 2020 and 2021. Dry-powder has increased by 53% within the first six months of 2021 alone. In addition, continuingly low interest rates may encourage funds to use more leverage to finance deals.

Investors are on the lookout for distressed opportunities all over Europe. NPLs can be debt-equity-swapped and thereby used as an acquisition tool for distressed investors. Modern “hybrid” proceedings like the new German StaRUG or the Dutch WHOA with their sophisticated cram-down mechanism can help investors safeguard the acquisition of control over a debtor in a court-supervised process. The crucial factor, however, will be whether valuations eventually come down to investable levels.

Summary

In this Insight, we have taken a closer look on the European NPL-Market. NPL-Trades have remained at an all-time low during the COVID-Crisis. However, experts predict rising NPL-Volumes while State-Aid-Programmes are slowly coming to an end. The EU aims to make the European NPL-Market more efficient and has identified the reduction and prevention of NPLs as a core-concern. Pressure from EU and domestic regulators on banks will rise. Distressed investors are sitting on huge piles of dry-powder while the expectation is that valuations may come down sooner rather than later. Innovative securitisation-schemes such as GACS and HAPS could be an efficient way to effectively manage NPL-Portfolios in the future. Lenders should start identifying the opportunities of an effective NPL management strategy and should start combing through their loan books for potential NPLs. All in all, the market for NPLs is gaining momentum.

1 ECB, Guidance to banks on non-performing loans, March 2017, Nr. 5.2.

2 EBA/GL/2018/06: Guidelines on management of non-performing and forborne exposures, Nr. 7.

3 BaFin, Rundschreiben 3/2019(BA).

4 In detail see Radünz, in: Köchling/Schalast, Grundlagen des NPL-Geschäfts, pp. 3

5 EBA/GL/2018/06: Guidelines on management of non-performing and forborne exposures, Nr. 7.

6 BaFin, Rundschreiben 3/2019(BA).

7 See infographic of the Federal Ministry for Economic Affairs and Climate Action, available at: https://www.bmwi.de/Redaktion/DE/Infografiken/Wirtschaft/corona-hilfen-fuer-unternehmen-marginalspalte-IG.html

8 PEPP is the pandemic emergency purchase programme by the ECB to address the serious risks to the monetary policy transmission mechanism posed by the COVID outbreak. Regarding an overview of the current holdings under the PEPP see: https://www.ecb.europa.eu/mopo/implement/pepp/html/index.en.html

9 Griess/Koß/Roessle, Ernst & Young, NPL Backstop, available under: https://www.ey.com/de_de/financial-services/npl-backstop-wie-banken-ihre-kreditrisiken-zugig-abbauen-konnen.

10 BKS, NPL-Barometer 2021, p. 7.

11 Section 1 of the German Short-Time Workers' Allowance Extension Regulation.

12 ECB, Press release dated 17 December 2021, available under: https://www.bankingsupervision.europa.eu/press/pr/date/2021/html/ssm.pr211217~39656a78e8.en.html

13 Tracey, Bank of England Staff Working Paper No. 783, The real effects of zombie lending in Europe, available under: https://www.bankofengland.co.uk/-/media/boe/files/working-paper/2019/the-real-effects-of-zombie-lending-in-europe.pdf.

14 Kearney, Einmal Zombie, immer Zombie?, July 2021, p. 1.

15 General criticism Hülsmann, Krise der Inflationskultur; recently Interview Hanno Lustig (Professor Stanford Graduate School of Business) with “Frankfurter Allgemeine Zeitung”, 14 December 2021, Nr. 291, p. 19.

16 See FED, Press release dated 15 December 2021, available under:

https://www.federalreserve.gov/newsevents/pressreleases/monetary20211215a.htm.

17 See Bank of England, Monetary Summary and minutes of the Monetary Policy Committee meeting published 16 December 2021, available under: https://www.bankofengland.co.uk/monetary-policy-summary-and-minutes/2021/december-2021.

18 See ECB, Press release dated 16 December 2021, available under:

https://www.ecb.europa.eu/press/pr/date/2021/html/ecb.mp211216~1b6d3a1fd8.en.html.

19 EU Commission, Action plan: Tackling non-performing loans (NPLs) in the aftermath of the COVID-19 pandemic, https://ec.europa.eu/info/publications/201216-non-performing-loans-action-plan_en.

20 Regulation (EU) 2019/630.

21 ECB, Communication on supervisory coverage expectations for NPEs, published 22 August 2020.

22 Commission Staff Working Paper, European Platform for Non-Performing Loans, SWD(2018), 472 final.

23 Art. 4 and Art. 13 Directive (EU) 2021/2167; see also Van Roosebeke, in: Köchling/Schalast, Grundlagen des NPL-Geschäfts, p. 75, 96.

24 Keibel, in: Köchling/Schalast, Grundlagen des NPL-Geschäfts, p. 433, 444.

25 Regulation (EU) 2021/557 amending Regulation (EU) 2017/2402 laying down a general framework for securitisation and creating a specific framework for simple, transparent and standardised securitisation to help the recovery in response of the COVID-19 crisis.

26 EU Commission, Press release, Action plan: Tackling non-performing loans (NPLs) to enable banks to support EU households and businesses, available under: https://ec.europa.eu/commission/presscorner/detail/en/ip_20_2375.

27 Doppstadt/Plagemann, in: Köchling/Schalast, Grundlagen des NPL-Geschäfts, pp. 391.

28 Interview Andrea Enria (Chair of the Supervisory Board of the ECB) with “Handelsblatt”, 12 October 2020, available under: https://www.bankingsupervision.europa.eu/press/interviews/date/2020/html/ssm.in201012~f68deb5173.en.html

29 See MaRisk 6. Novelle, BTO part nr. 3; EBA/GL/2018/06: Guidelines on management of non-performing and forborne exposures, Nr. 5.2.1 part nr. 63; ECB, Guidance to banks on non-performing loans, Nr. 3.3.1.

30 MaRisk 6. Novelle, AT 9 part nr. 4; EBA/GL/2019/02, Nr. 4.

31 Regulation (EU) 2021/557 amending Regulation (EU) 2017/2402 laying down a general framework for securitisation and creating a specific framework for simple, transparent and standardised securitisation to help the recovery in response of the COVID-19 crisis.

32 Regulation (EU) 2021/558 amending Regulation (EU) 575/2013 as regards adjustments to the securitisation framework to support the economic recovery in response of the COVID-19 crisis.

_11zon.jpg?crop=300,495&format=webply&auto=webp)