Implementation of ATAD in Germany

Changes to German CFC-Rules relevant to asset managers.

Background

The Anti-Tax-Avoidance-Directive (“ATAD”) (Council Directive (EU) 2016/1164) obliges EU member states to implement into national law the minimum standards contained in the directive, including rules for controlled foreign companies (“CFC-Rules”). The directive was required to be transposed into national law by 31 December 2019.

On 24 March 2021, the German Federal Government approved a draft law (“Draft law”) to implement ATAD into national law (“ATAD Implementation Law”). A key component of this Draft Law is the reform of the German Foreign Tax Act (Außensteuergesetz) (“AStG”) with regard to the taxation of income under the German CFC-Rules. The reform of the CFC-Rules involves a change from a German domestic control concept to a shareholder-based approach, taking into account related parties.

Up until now, if the German Investment Tax Act (Investmentsteuergesetz) (“InvTA”) applies to an investment fund, the application of the CFC-Rules is generally excluded. However, even though the ATAD Implementation Law does not abolish this rule, under its current wording the protection of the InvTA may no longer apply in certain situations, explained below.

Currently Applicable CFC-Rules

Under the current CFC-Rules, German tax resident shareholders ("German Shareholders") could be subject to taxation on the income of a CFC, if:

German Shareholders (regardless of whether they are related or not) hold a stake of more than 50% (shares or voting rights) in the CFC (domestic control);

the CFC realises passive income (eg interest income); and

this income is subject to taxation at a rate of less than 25% (low taxed income).

If this is the case, the passive low taxed income of the CFC is attributed to the German Shareholders irrespective of a distribution.

Passive Income

Passive income means any income of the CFC which is not listed in Section 8 para. 1 AStG as active income. Typical examples of passive (non-active) income are interest or other income from capital realised not as part of the business operations of a corporation. This means that eg interest received by a bank with substance (employees, office etc) is not passive, but interest income of a (holding) company with no relevant substance usually is. However, dividend income until now qualifies as active income and capital gains realised upon the disposal of shares qualifies as active income if the shares sold are those of an "active" company.

Income allocation under CFC-Rules

Income allocated to German (indirect) Shareholders under the CFC-Rules is deemed to be distributed on the first day following the end of the business year of the CFC. It is always fully subject to tax (eg the participation exemption for dividends does not apply) and no preferential tax rates apply. Later actual distributions are, very broadly, tax exempt to the extent they do not exceed the allocations under the CFC-Rules.

Tax filing obligations

Under the CFC-Rules affected German Shareholder must file a declaration for a separate determination of the CFC income allocated to them. If a German Shareholder is not the only investor tax resident in Germany, a so called separate and uniform tax return must be filed with the German tax authorities by and for the German Shareholders.

Lower tier CFCs

If a German Shareholder invests in a CFC (upper tier company), which, either alone or together with other shareholders, holds an interest in another CFC (lower tier company), then for purposes of applying the CFC-Rules, the passive income of the lower tier company that has been subject to low taxation will be allocated to the upper tier company in proportion to its ownership in the lower tier company's nominal capital (a so-called "transferring attribution") (übertragende Zurechnung). Thus, in this case, the income of the lower tier company is attributed to the upper tier CFC and then the aggregated passive low-taxed income is attributed to the German Shareholder (via the upper tier CFC).

Exception for investment funds

Pursuant to Section 7 para. 7 AStG, the CFC-Rules do not apply if the rules of the InvTA are applicable, which is generally the case for all funds (AIFs within the meaning of the German Capital Investment Code - Kapitalanlagegesetzbuch) which are not organised as partnerships. This equally applies for the purposes of the rules applicable to transferring attributions from a lower tier CFC.

Lower holding requirements for CFCs which realise income from capital investments

However, if the CFC realises income from capital investments (Einkünfte mit Kapitalanlagecharakter, such as interest income, but not dividend income), no "German" control of the CFC may be necessary for the application of the CFC-Rules. This rule is particularly relevant in the case of investments in foreign funds, since in most cases German investors will not have control of a fund.

Contemplated Changes

Change from a domestic control to a shareholder-based approach

Pursuant to the Draft Law, a German Shareholder may be subject to the CFC-Rules if he controls the CFC. The income is allocated to the German Shareholder in proportion to its direct and indirect participation in the nominal capital of the CFC. This is a crucial change to the currently applicable CFC-Rules, which require control by German shareholders (which can be unrelated). So the change restricts the scope of the CFC-Rules to a situation where a German shareholder and related parties control the CFC. It is no longer enough for unrelated German Shareholders to hold 50% or more.

Control exists if more than 50% of the shares or voting rights in the nominal capital are directly or indirectly attributable to the German Shareholder alone or jointly with related parties, or if the German Shareholder is directly or indirectly entitled to more than half of the profits or liquidation proceeds of that company at the end of the fiscal year.

According to the Draft Law, a person will be considered to be a related party if it acts in concert with the German Shareholder in relation to the CFC. In the case of direct or indirect partners in a partnership which is directly or indirectly participating in a CFC, co-operation through acting in concert is refutably presumed. Unfortunately, the legislator has not given any examples how this legal presumption can be rebutted. This rule, if enacted, will have implications for commonly used fund structures organised as partnerships.

No changes regarding the precedence of the InvTA over the CFC-Rules

According to the Draft Law, the CFC-Rules would, as under currently applicable law, remain excluded if the InvTA applies. Thus, for income realised directly (and not via subsidiaries) by an investment fund, the CFC-Rules continue to be excluded. However, the Draft Law provides an exception to this rule if more than one-third of the activities on which the income of the investment fund is based are carried out with the German Shareholder or parties related to this shareholder.

No changes regarding CFCs which realise income from capital investments

The rules for CFCs which realise income from capital investments will generally remain unchanged. Accordingly, in such cases, control of the CFC remains unnecessary for the application of the CFC-Rules. However, this rule remains excluded where the InvTA applies. Those benefiting from this precedence rule include, for example, German investors in UCITS investing into bonds or debt funds which directly receive interest from the loans they issue. Furthermore, this rule shall also be excluded for companies which are held indirectly via an investment fund on which the InvTA applies.

Changes in relation to lower tier CFCs

The Draft Law no longer contains the concept of the transferring attribution (übertragende Zurechnung). Rather, the income of the lower tier CFC will become directly attributable to an indirect German Shareholder.

No changes regarding the relevant tax rate

Contrary to market expectations, the tax rate for assessing what amounts to "low taxation" will not be reduced, but will remain at "less than 25%", which means that most countries in the world will have tax rates which may cause the application of the CFC-Rules.

Adjustments to the passive income definition

One of the main criteria for the application of the CFC-Rules is the realisation of passive income through the CFC. The AStG contains an exclusive list of active income that is not subject to the CFC-Rules.

The ATAD, on the other hand, defines harmful (passive) income as including (a) interest or other income from financial investments, (b) royalty payments or other income from intangible property rights and (c) dividends and capital gains from the sale of shares.

Under the Draft Law, the list of active income remains. However, the proposed amendments take up concepts from the ATAD. Relevant for asset managers are, in particular, the following points:

Rental income remains generally active subject to the current exceptions.

Dividend income will continue to qualify as active income. However, dividends will - contrary to the current rule - no longer qualify as active income if:

- the distribution has reduced the income of the paying corporation (with some exceptions);

- there would be a tax liability in Germany under section 8b para. 4 of the German Corporate Income Tax Act, ie essentially if the shareholding is less than 10%; or

- a tax liability would exist in Germany pursuant to section 8b para. 7 German Corporate Income Tax Act, ie essentially in the case of shares held in the trading book of credit or financial services institutions.

Capital gains from the sale of shares continue to qualify as active income as far as they are not subject to taxation pursuant to section 8b para. 7 German Corporate Income Tax Act.

Examples

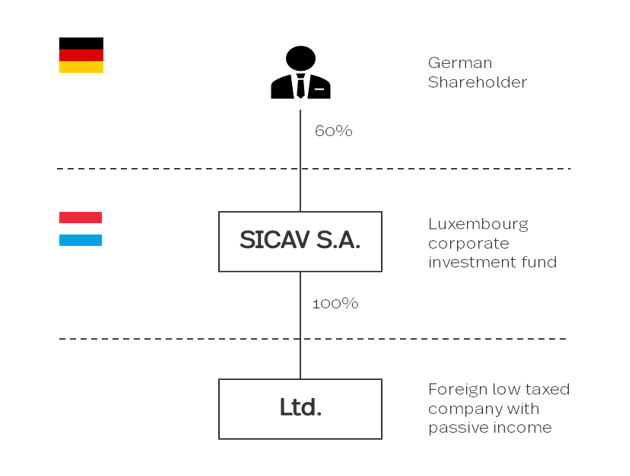

Scenario 1

A. Current CFC-Rules

The application of the CFC-Rules is excluded since the InvTA is applicable.

B. Amended CFC-Rules

For the purposes of the German CFC-Rules, the participation of SICAV S.A. in the Ltd. is now attributable to the German Shareholder in proportion to its shareholding of 60% since the Draft Law also covers indirect participations, ie 60% of the passive income of the Ltd. will be attributed to the German Shareholder directly irrespective of any distribution.

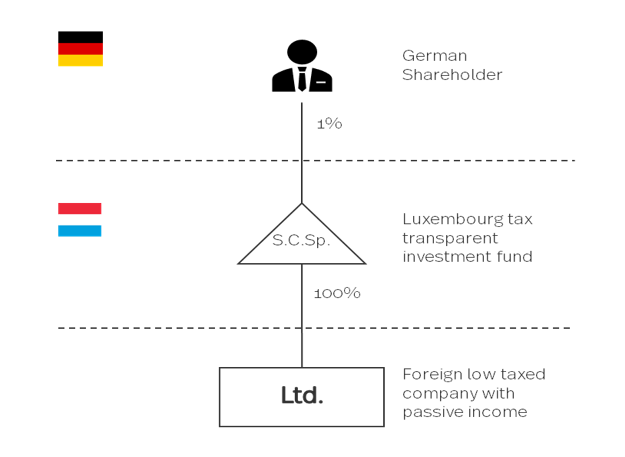

Scenario 2

A. Current CFC-Rules

The direct participation of the German Shareholder in the S.C.Sp., which is transparent for tax purposes, is less than 50%. Therefore, under the current CFC-Rules the passive income of the low taxed Ltd. would generally not be allocated to the German Shareholder (unless the Ltd. generates income from capital investments (Zwischeneinkünfte mit Kapitalanlagecharakter).

B. Amended CFC-Rules

Under the amended CFC-Rules, there would also generally be no attribution of the passive income of the Ltd. to the German Shareholder, as the indirect shareholding does not constitute a shareholding of more than 50%.

However, since the German Shareholder is a partner in a partnership (the S.C.Sp.), pursuant to the Draft Law it is refutably presumed that the German Shareholder and the other investors of the S.C.Sp. are acting in concert and are controlling the Ltd. Thus, the passive income of the Ltd. may be attributable to the German Shareholder.

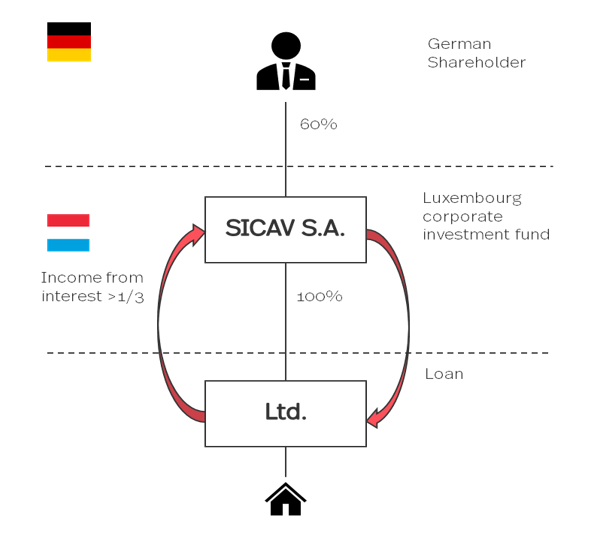

Scenario 3

A. Current CFC-Rules

The application of the CFC-Rules is excluded since the InvTA is applicable.

B. Amended CFC-Rules

Under the Draft Law, the application of the CFC-Rules would no longer be excluded since (i) the Ltd. is a related party to the German Shareholder because of its indirect 60% participation, (ii) the interest income from the shareholder loan to the Ltd. amounts to more than one-third of the income of the SICAV S.A. and (iii) the interest income qualifies as passive income. Therefore, the interest income from the shareholder loan may be attributable to the German Shareholder.