ISDA publishes IBOR Fallbacks Supplement and Protocol

On 23 October 2020, ISDA published its IBOR Fallbacks Protocol and Supplement, which becomes effective on 25 January 2021. The Protocol is open for adherence.

Background and Overview

The ISDA 2020 IBOR Fallbacks Protocol (the "Protocol") and ISDA IBOR Fallbacks Supplement (the "Supplement") have been much anticipated as they provide a global mechanism for the replacement of the current fallbacks in certain ISDA and non-ISDA agreements which are no longer fit for purpose.

Existing fallbacks do not contemplate a permanent cessation of the rate options used to calculate the floating amount payable in respect of a transaction. This is primarily because, where a rate option is unavailable, these fallbacks typically require the relevant party to obtain quotes from reference banks in the relevant market. However, banks are unlikely to be willing to provide these quotes if the relevant rate option is no longer published or is declared unrepresentative.

New Transactions (Supplement)

The Supplement amends the 2006 ISDA Definitions by introducing new fallbacks in contemplation of the cessation of any of the following rate options (each, for the purposes of this article, an "IBOR"). These amendments automatically apply to uncleared derivatives contracts that incorporate the 2006 ISDA Definitions and are entered into on or after 25 January 2021.

- Sterling London Interbank Offered Rate (GBP-LIBOR)

- Swiss Franc London Interbank Offered Rate (CHF-LIBOR)

- U.S. Dollar London Interbank Offered Rate (USD-LIBOR)

- Euro London Interbank Offered Rate (EUR-LIBOR)

- Japanese Yen London Interbank Offered Rate (JPY-LIBOR)

- Euro Interbank Offered Rate (EUR IBOR)

- Japanese Yen Tokyo Interbank Offered Rate (TIBOR)

- Euroyen Tokyo Interbank Offered Rate (Euroyen TIBOR)

- Bank Bill Swap Rate (BBSW)

- Canadian Dollar Offered Rate (CDOR)

- Hong Kong Interbank Offered Rate (HIBOR)

- Singapore Dollar Swap Offer Rate (SOR)

- Thai Baht Interest Rate Fixing (THBFIX)

- London Interbank Offered Rate (with no reference to a specific currency)

Existing Transactions (Protocol)

On the other hand, the Protocol addresses legacy OTC derivatives master agreements, credit support documents and related confirmations that:

incorporate the 1991 ISDA Definitions (as amended by the 1998 Supplement), 1998 ISDA Euro Definitions, 2000 ISDA Definitions and 2006 ISDA Definitions;

reference a rate 'as defined in' any of these ISDA Definitions; or

otherwise reference any of the IBORs listed above;

and were entered into prior to 25 January 2021, or if later, the date ISDA accepts the adherence letter of the second party to adhere.

(each a "Protocol Covered Document").

The Protocol is also hard-wired to apply to certain specified non-ISDA master agreements (of which there are 74) and credit support documents (of which there are 7) that do not incorporate the ISDA Definitions but do reference IBORs (each an "Additional Protocol Covered Document"). These include the following agreements:

2000 TBMA/ISMA Global Master Repurchase Agreement (GMRA);

2011 SIFMA/ICMA Global Master Repurchase Agreement (GMRA);

2010 ISLA Global Master Securities Lending Agreement (GMSLA);

2018 ISLA Global Master Securities Lending Agreement (GMSLA) - Security Interest over Collateral; and

1996 TBMA Master Repurchase Agreement (MRA).

The full list of Additional Protocol Covered Documents is set out in an annex to the Protocol. Firms will need to check whether all their relevant trading documents that reference IBORs are covered by this list. For instance, one notable omission is the German Master Agreement for Financial Derivatives Transactions (Rahmenvertrag für Finanztermingeschäfte - DRV).

To the extent firms require exclusions / additions to the list of Additional Protocol Covered Documents, these will need to be agreed bilaterally. ISDA has published template language that can be used for these purposes.

Triggers and fallbacks

The Protocol and Supplement has in part been drafted to take account of the EU Benchmark Regulation1 (the "BMR"). Article 28(2) of the BMR requires supervised entities (a term which includes AIFMs, MiFID investment firms and UCITS) that "use a benchmark" to produce and maintain "robust written plans" setting out the actions they would take in the event that a benchmark materially changes or ceases to be provided.

Where feasible and appropriate, the plans must nominate one or several alternative benchmarks that could be referenced to substitute unavailable benchmarks, and be reflected in a firm's contractual relationships. To this end, the Protocol and Supplement introduces a waterfall of fallback rate options that will apply in the event of the temporary unavailability or cessation of an IBOR.

Temporary unavailability

The following waterfall of fallbacks will apply in respect of any temporarily unavailable IBOR:

initial fallback to the rate for the swap's reset date provided by the administrator,

if the rate in (1) is unavailable by a specified time, the rate recommended by that rate's administrator or if not available, its supervisor; and

if the rate in (2) is unavailable by a specified time, the alternative determined by the Calculation Agent in a commercially reasonable manner.

Index Cessation Events

The Protocol and Supplement distinguishes between (i) pre-cessation (for LIBORs in GBP, EUR, USD, CHF and JPY, as well as SOR and THB-FIX) and (ii) permanent cessation (for all relevant IBORs), and introduces new fallbacks in respect of each type of event.

Pre-Cessation Event

A Pre-Cessation Event is relevant only to LIBORs in GBP, EUR, USD, CHF and JPY, as well as SOR and THB-FIX (the latter two because USD-LIBOR is used as an input to calculate these rates). It occurs if there is a publication by the regulatory supervisor for the administrator of LIBOR (ie the UK's Financial Conduct Authority) announcing that:LIBOR in the relevant currency is no longer capable of being representative (or as of a specified future date will no longer be) or is non-representative of the underlying market and economic reality that it is intended to measure, as required by applicable law or regulation or as determined by the regulatory supervisor in accordance with applicable law or regulation; and

the intention of that publication is to engage contractual triggers for fallbacks activated by such pre-cessation announcements.

It is important to note that the pre-cessation fallbacks in the Protocol and Supplement will only become effective (a) upon that IBOR no longer being provided; or if sooner, (b) upon the first date that IBOR is non-representative, as set out in the announcement published by the regulatory supervisor or administrator of that IBOR.

This means that there could be an interval of time between the occurrence of a Pre-Cessation Event (ie the FCA's announcement) and the application of the relevant fallbacks in the Protocol and Supplement. For example, an announcement by the FCA in December 2020 that LIBOR will no longer be representative of the underlying market as of 31 December 2021 will mean that the fallbacks in the Protocol only apply on 31 December 2021.

The FCA has previously indicated that announcements of unrepresentativeness could be expected as early as November or December 2020, although it is unclear whether this timing might be impacted as a result of the delayed publication of the Protocol and Supplement.

Permanent Cessation Event

A Permanent Cessation Event will occur upon a publication by the administrator of the relevant IBOR, its regulatory supervisor, or an insolvency official or resolution authority with jurisdiction over the administrator, announcing that it has ceased or will cease to provide that IBOR permanently or indefinitely, provided that there is no successor administrator that will continue to provide the relevant IBOR at the time of the announcement.

The relevant fallbacks in the Protocol and Supplement will only become effective upon the first date that IBOR is no longer provided, so as above, there could be an interval of time between the occurrence of a Permanent Cessation Event and the application of the relevant fallbacks.

On the effective date of an index cessation event, the Protocol and Supplement applies an initial fallback that is published or distributed by Bloomberg, its authorised distributors or its successor (the "Fallback RFR Rates"). Further fallbacks apply in the event of the temporary availability of a Fallback RFR Rate or an index cessation effective date in respect of that rate. The waterfall of fallbacks for GBP-LIBOR, EUR-LIBOR and USD-LIBOR are appended below.

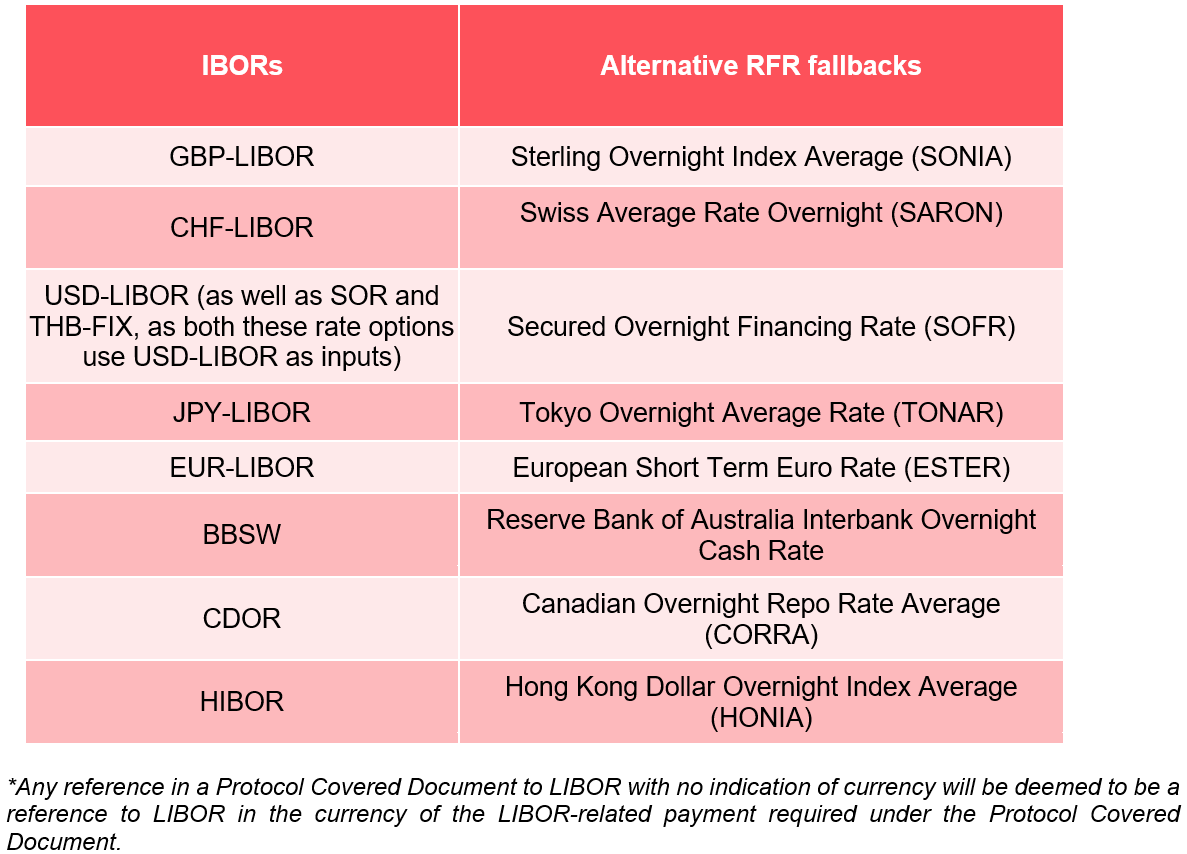

What are the Fallback RFR Rates?

Following several market consultations, ISDA concluded that IBORs should be replaced by certain risk-free rates ("RFRs") that are adjusted to address the structural differences between IBORs and RFRs. The table below sets out the RFRs identified by the relevant public / private sector working groups for this purpose:

RFRs are structurally different from IBORs in that they are overnight rates instead of being available in various tenors, are backward-looking instead of forward-looking, and do not price in term bank credit risk or a liquidity premium for longer term funding. As such, each Fallback RFR Rate is calculated by (i) term-adjusting the relevant RFR for the tenor of the IBORs they replace, and (ii) adding a spread equivalent to the median over a 5-year period of the historical differences between the IBOR in the relevant tenor and the relevant RFR compounded over the corresponding term, up to the date no later than two business days prior to the date of the relevant cessation statement or publication. Bloomberg has been appointed to publish the term-adjusted RFRs, spread and the "all-in" Fallback RFR Rate comprising the term-adjusted RFR and spread, and has been doing so since July 2020 on an indicative basis.

However, it is important to note that the spread published by Bloomberg will only crystallise on the date of the first public statement or publication of information which constitutes an index cessation event. This means that, whilst there may be an interval of time between an index cessation event in respect of an IBOR and when the corresponding Fallback RFR Rate actually replaces it, the spread that forms part of that Fallback RFR Rate is fixed on the date an index cessation event occurs (ie the date that the FCA declares LIBOR unrepresentative or the date on which the permanent cessation of an IBOR is announced).

What are the practicalities of Protocol adherence / incorporation?

As the Supplement applies automatically to new trades entered into on or after 25 January 2021, market participants need only consider how they plan to amend trades entered into prior to that date. If market participants choose to use the Protocol mechanism, the choice is between adherence to the Protocol and incorporation of the Protocol into their bilateral agreements.

Bilateral amendments to the Protocol

Bilateral incorporation of the Protocol leaves scope for the parties to tailor the terms of the Protocol to their requirements, by excluding documents from or adding documents to the scope of the Protocol, disapplying the pre-cessation fallbacks, and/or making any other amendments (for example, to include a dispute resolution process in respect of determinations made by the calculation agent).

There is no scope to make such amendments if a party chooses to adhere to the Protocol on ISDA's website.

Adherence to the Protocol as agent

The Protocol allows a party to adhere as agent on behalf of its clients, even where it has not entered into the relevant agreements as agent on behalf of its clients. A party that intends to do so is required to provide the counterparty to the agreement with reasonable evidence of its authority to amend those agreements, within 15 days of that counterparty's request.

This mechanism resolves the argument that the agent does not have the requisite authority to bind its client(s) through its Protocol adherence where it has not entered into its clients' agreements as agent - an issue that has been raised in respect of agency adherence to past ISDA protocols.

Consents / formalities in respect of credit support documents

The Protocol requires an adhering party to undertake that it has obtained any necessary third party consents or approvals in respect of third party credit support documents that support a Protocol Covered Document, as a consequence of the amendments made by the Protocol to that document. Parties are also required to provide evidence of these consents if requested.

Parties should therefore consider whether they have obtained any third party consents that may be required to amend such credit support documents, and whether they need to take any steps to satisfy any formalities (such as the retaking of security) in respect of credit support documents that will be directly amended by the IBOR Fallbacks Protocol.

Costs

The one-time cost of adhering to the Protocol is USD $500, except that this cost is waived for a party that is not an ISDA Primary Member and adheres to the Protocol before 25 January 2021.

How does the Protocol/Supplement fit in with other benchmark reform initiatives?

The Protocol and Supplement complements a wider raft of measures taken by ISDA to effect benchmark reform.

The Benchmarks Regulation

As mentioned above, Protocol adherence has been identified as one way of fulfilling the regulatory requirement under Article 28(2) of the EU Benchmarks Regulation for supervised firms in the EU to have robust written plans addressing a cessation of or material change to a benchmark.

Another mechanism previously developed as a means for market participants to comply with the Article 28(2) requirement is the Benchmarks Protocol and Supplement published by ISDA in late 2018. The Benchmarks Protocol and Supplement introduces generic fallbacks for benchmarks that do not have their own fallbacks. Whilst the specific fallbacks in the IBOR Fallbacks Protocol and Supplement take precedence over these generic fallbacks once effective, the Benchmarks Supplement covers a wider range of benchmarks than the IBOR Fallbacks Protocol and Supplement, and provides additional fallbacks in the event a benchmark or its administrator is not authorised or approved.

Separately, the European Commission has also proposed that it is given power under the EU Benchmarks Regulation to designate a replacement benchmark for existing financial instruments, contracts and performance measures for investment funds that do not contain any suitable fallbacks. That draft is still going through the EU legislative process but, as currently drafted, the proposal would allow references to a discontinued or non-representative benchmark in a relevant contract to be replaced by operation of law, without further action by the contracting parties. At this stage, it is unclear how the proposal will interact with the FCA's "Tough Legacy" powers (as described below), or other legislative powers that regulators in other jurisdictions may seek to exercise to ease the transition of IBORs.

Tough Legacy Contracts

Whilst it is intended that the Protocol and Supplement will address the IBOR transition risk in the bulk of derivatives contracts, they cannot resolve risk in contracts where it may not be as easy or possible to amend existing fallback provisions (so-called "Tough Legacy" contracts). These contracts include non-linear derivatives contracts (such as derivatives that are used to hedge exposures that might have Tough Legacy characteristics, or derivatives that form part of a more complex structure), bonds, syndicated and bilateral loans, and mortgages.

To address the risk in Tough Legacy LIBOR contracts, the UK government announced that it intends to amend the UK version of the Benchmarks Regulation to give the FCA enhanced powers to change the methodology used to determine LIBOR, thereby producing a 'synthetic' form of LIBOR, if allowing the limited use of LIBOR during the LIBOR transition period would 'protect consumers and market integrity'. However, the FCA has made very clear that it will only use these powers as a last resort, and that it is more likely to use these powers to address Tough Legacy contracts if there is widespread uptake of the Protocol.

Interest Rates in Collateral Agreements

ISDA has also produced versions of its Collateral Agreement Interest Rate Definitions, which include fallbacks that will apply in the event of a permanent discontinuation of a benchmark referenced as the interest rate (or forming part thereof) in collateral agreements, as well as bilateral templates that allow parties to amend references to EUR and/or USD interest rates in collateral agreements to EuroSTR and SOFR.

Should you adhere to the Protocol?

Whilst adherence to the Protocol is, as always, voluntary, regulators have made strong statements encouraging adherence. The FCA stated on 3 August 2020 that any UK regulated firm with large uncleared derivatives exposures that chooses not to adhere 'will need to be ready for some serious questions ...on how [they] will mitigate [the] risks" of a cessation of or material change in a benchmark like LIBOR. The Bank of England's Working Group on Sterling Risk-Free Reference Rates and the Alternative Reference Rates Committee, (which is convened by the U.S. Federal Reserve Board and the New York Fed) have both issued statements recommending adherence of the Protocol before its effective date of 25 January 2021. The European Supervisory Authorities, the CFTC and the Prudential Regulation Authority have also given market participants further comfort by making clear that amendments to legacy contracts for the purposes of replacing IBORs with RFRs will not trigger clearing or margining requirements in their jurisdictions.

Firms should consider the Protocol in detail and assess its compatibility with their derivatives arrangements, particularly where there is any concern about hedging mismatches and accounting, tax and regulatory issues arising from the transition from IBORs to structurally different RFRs. In particular, firms should assess whether they are comfortable with the calculation methodology of the Fallback RFR Rate, bearing in mind that, at the time of adherence, parties will not know what the spread element of the Fallback RFR Rate will be until an index cessation event occurs.

If firms are comfortable with the Protocol mechanism, they should also consider whether they wish to adhere to the Protocol or incorporate the Protocol (and any amendments they wish to include) on a bilateral basis. Finally, firms may also wish to consider their response to the various benchmark reform initiatives as a whole, in order to formulate a coherent and consistent approach across all aspects of their documentation and trading.

Further information

> IBOR Protocol Waterfalls - Flowcharts

Should you require further information or advice on the application of the Supplement and/or Protocol, please reach out to any of the listed contacts or your usual Simmons & Simmons contact.

1Regulation (EU) 2016/1011 of the European Parliament and the Council of 8 June 2016

_11zon.jpg?crop=300,495&format=webply&auto=webp)

.jpg?crop=300,495&format=webply&auto=webp)