General Election Update - Labour Intensive 05 December 2019

Financial markets, particularly utility prices, appear to have dismissed almost completely the scenario around a Labour-led administration.

Our scenario analysis uses a number of different indicators sensitive to different aspects of the scenarios. We call these short-term indicators our ‘canaries’ – a reference to their use as warning signs in the early years of the mining industry. Our normally consistent group is beginning to give different answers; time to check inside their gilded cage.

Financial market canaries: mostly singing in a cheerful major key

For the General Election 2019 scenario analysis we use three canaries from financial markets:

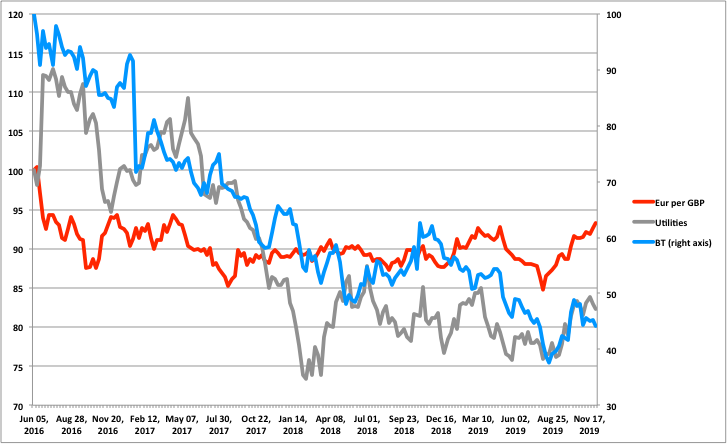

- the value of the FTSE 350 Gas and Multi-Utilities Index as a particular test of sentiment towards a Labour administration given the obvious sensitivity to Labour’s nationalisation plans

- the value of shares in BT Group as a further test on perceptions around Labour given its proposals to nationalize BT’s broadband operations

- the value of sterling against the euro as an indicator of general risk sentiment but unable to distinguish between the perceived risk of a Hard Brexit or a Labour-led administration (despite the IFS pointing to a 5% difference in GDP between the two outcomes in favour of the Labour-led administration)

The two utilities (broad index and BT) have had a torrid time (more accurately their shareholders) since long before the June 2017 election and the publication of the Labour Party manifesto for that election which carried the first formal articulation of its nationalisation ambitions.

Those torrid times seem unlikely to have been caused by the 2017 Labour manifesto – Labour was not in power. Rather it may have had more to do with Theresa May adopting populist measures to similar effect: the energy price cap and the nationalisation of the East Coast rail franchise in 2018.

But since Johnson became Prime Minister in July 2019 both the broad Utilities index and the BT share price have rallied by 10% and 20% respectively – in the case of BT that’s despite the recent about proposal by Labour to nationalize its Openreach broadband operations.

Our third canary from financial markets, the value of sterling against the euro, has rallied strongly since Johnson became leader of the Conservative Party back in July rising not only by 9% but, more importantly, to levels not seen since the relatively halcyon days of Theresa May’s Lancaster House address in January 2017.

Given that the utility prices seem to have discounted the perceived risk of a Labour administration it seems reasonable to conclude the same for the rally in sterling – that investors in UK assets have dropped any demanded risk premium that might have been attached to Labour’s full policy programme.

Two minority scenarios remain: Labour-led alliance and Hard Brexit

But that leaves two residual, minority scenarios. We have spoken before about the scenario of a Labour-led rainbow coalition of sorts and despite protestations around the personality politics at the top of the different parties a Labour minority government remains a 25% probability among pollsters and punters at the bookies!

The other residual risk is that of Hard Brexit. If Johnson wins with a comfortable majority he will be able not only to deliver the UK’s formal exit from the EU by January 31st but also to ‘take a view’ on the pace/ progress of negotiations towards an EU-UK FTA including the possibility to walk away without an FTA on December 31st, 2020. But that risk seems also to have been priced by sterling as minimal given that its value is already back to ‘Lancaster House’ days and that Johnson’s WAB is regarded as less economically benign than Theresa May’s. Our own calculations suggest still a 25% chance of Hard Brexit following a Johnson majority. Financial markets may, in the historic words of Alan Greenspan, be suffering an outbreak of “irrational exuberance” if they are truly discounting the risk of Hard Brexit

Opinion poll canaries: some darker tones in minor keys

We have reviewed those in some detail in previous updates and the picture remains as it has become in recent days: volatile. The latest poll-of-polls average has a less than 10% difference between Conservatives and Labour with LibDems trailing by some distance on less than 13% and the Brexit Party, king-makers (for Johnson) in their own demise, on 3%.

Those polls project a majority of 28 for Johnson – a long way down from the 70+ numbers at the start of the campaign but still healthy enough to prosecute his Brexit agenda and deliver a new Queen’s Speech and February Budget.

The headline we referred to earlier (“just a normal poll error away from a Labour government”) was prompted by a particular poll showing the poll gap reduced to 7% and a projected ‘majority’ of -2. It is an example of course of poetic licence; but it makes the point that the polls are now in the territory where small differences have large consequences. And in that observation these opinion poll canaries sing a somewhat more nuanced song, in minor keys, compared to their financial market cousins

If a week is a long time in politics under normal circumstances it must be an eternity in the closing stages of the most polarized election campaign in living memory. The Sunday newspapers to be published this weekend may be the most influential for many decades in determining the final outturn of this campaign.

Scenario characteristics and implications

A Labour Majority government is not included among the scenarios here given its chances, according to Prof. Sir John Curtis, are ‘close to zero’. Other indicators we track point to the same conclusion. Even so we will continue to monitor the possibility. For the other possible/ more likely outcomes, here’s what we see as the characteristics, chances and implications of each one.

Conservative majority (64% - modestly lower)

To be clear we mean a working majority without requiring the formal support of any other party. While the collapse of the Brexit Party vote share (down from over 20% to less than 4%) has unsurprisingly worked to Mr. Johnson’s advantage we note (see earlier) the wide volatility now in projected seats with some suggestion of a tendency towards smaller projected majorities since the publication of all manifestos.

Conservative majority: Brexit Implications – Hard Brexit not off the table

Johnson pushes through his WAB by 31 January 2020; European Communities Act repealed 11pm on the same day. UK ‘leaves’ EU at that moment. FTA negotiations begin with EU with UK-USA FTA discussions not far behind.

But, and proportionately to the size of majority, there would still be a risk of a No Deal Brexit, possibly even before 31 January (abandon the WAB) or, perhaps more likely, in the Transition period. The value of sterling versus the euro (recently €1.17) appears to suggest an almost 30% chance still of Hard Brexit.

Signals to look for

The bigger Johnson’s majority the greater his ability to play hard ball. For example, at the time of writing, the UK has still not appointed its EU Commissioner potentially delaying the start of the new European Commission until February 1st, 2020.

If the UK does ‘Brexit’ on/ before 31 January one of the next milestones will be July 1st – the deadline to request an extension to the Transition Period by up to 2 years. Will he request one? If not, are negotiations going so well that everyone is realistically confident an FTA will be concluded by 31 Dec 2020? If the answer to both is ‘No’ then a ‘No Deal’ Brexit looms by the end of 2020.

Note that, even in the event the UK leaves on ‘WTO terms’, Northern Ireland will, according to Johnson’s WAB, continue to operate under the WAB protocol requiring a dual tariff regime - one between NI and Ireland and the other between NI and GB – for at least 4 years until the Northern Ireland Assembly votes by simple majority to end the arrangement. Could this be an area in which Johnson might play hard ball using his working majority?

Conservative minority (1% - previously noted as less than 10%)

Johnson as PM sustained in power by the DUP – he’s unlikely to find support elsewhere and even this might be challenging given his apparent abandonment of the DUP in finalising his plans for the Northern Ireland border and future consent to continue with the arrangement.

Conservative minority: Brexit implications

More of the same before the GE depending on how far short of a majority he is. The DUP may be reluctant to forget their treatment during the WAB discussions so creating potential room for other parties to press parts of their election manifestos into the mix (but only for the Political Declaration (PD) not to re-open the WAB).

Still a likely Brexit on 31 January (but not before) and less likelihood (but not zero chance) of ending the FTA Transition Period with ‘No Deal’ on 31 Dec 2020.

Labour minority (25% - previously noted as less than 22%)

Perhaps the most problematic to contemplate given the principal challenge inherent in any conversation about a Labour-led minority government: the personality politics between Mr. Corbyn and the heads of the other parties.

If that became an impasse to forming a government after the GE (Friday 13th) could the Labour Party processes and personalities allow for a pragmatic and speedy change of leader? Could a Queen’s Speech be drafted say by Sir Keir Starmer?

All of which said and somewhat enigmatically, the bookies still have Corbyn as 25% favourite to be the “next PM”!

Labour minority: Brexit implications

All change! Johnson’s WAB would not be brought back to the House of Commons and the first order of business would be to seek another A50 extension to allow for a renegotiation of the WAB/ PD and a confirmatory referendum.

The bookies now have a 40% chance of such a referendum in 2020 – almost double the reading from last week. While the logistical challenges of organising a referendum on a new deal still to be negotiated makes that seem an optimistic timetable it is nonetheless consistent with the firming of probabilities around a Labour-led minority government noted above.

We conclude this section having seen a firmer view emerge this week around the chance of a Labour-led minority government in which Labour Party policy proposals could find expression, in direction if not degree, with the other opposition parties and still be transformational for the UK. In the following sections we examine some of the significant issues that could be raised for clients.

The issues raised for: Taxation

Labour’s 2019 Manifesto sets out a broad framework for a significant redesign of the UK tax regime - rebalancing as they would see it from taxation of labour to taxation of capital. Notable proposals include:

- increases in personal and business taxes

- extension of the existing General Anti-Abuse Rule into a broader General Anti-Avoidance Rule

- targeting perceived loopholes (such as the taxation regime applicable to carried interest)

- extension of stamp duty to a broader financial transaction tax, and

- proposal for inclusive-ownership funds

- a novel approach to generating additional tax revenues, through dividends paid by relevant companies that exceed £500 per employee being passed to the Treasury.

Please see our sister article for further details of the Labour Party tax proposals with a comparison to those of the Conservative and Liberal Democrat parties

The issues raised for: Real Estate

Although not an official Labour policy document, the “Land for the Many” report issued in June 2019 contains a broad series of recommendations to reform how what is referred to as “our fundamental asset” is used, owned and governed. We expect many of its proposals to be adopted in any future Labour Party manifesto at the next General Election.

Amongst the proposals, we see significant reforms to property taxation through:

- the replacement of council tax with a “progressive property tax”

- targeting owners not occupiers, and

- tackling empty or second homes, investment properties and non-resident owners.

- business rates could be replaced by a land value tax

- based on the rental value of local commercial land

- stamp duty land tax would be phased out for primary residences

- but retained for second homes and investment properties, and

- in addition, capital gains tax rates for second homes and investment properties would be aligned with income tax rates

- new lifetime gifts tax would replace the current inheritance tax regime and related real estate exemptions and reliefs.

Alongside the tax proposals, there would also be systemic reform. As a number of the tax proposals may affect house prices due to their impact on buy-to-let and similar investors, a novel “Common Ground Trust” has been mooted, a non-profit organisation that would stabilise prices whilst providing a mechanism for prospective purchasers to buy their homes in a more affordable way.

And at a macro-economic level, the Bank of England will be tasked with targeting house price inflation, to enable wages to catch up as house prices stabilise. We also see a greater focus on local issues, including community ownership of land, and a democratisation of real estate through measures such as an expanded right to roam.

The issues raised for: The Nationalisation Agenda and Public Services

The Labour Party Manifesto 2019 builds on its 2017 version and subsequent policy proposals which we have tracked and analysed throughout. There is relatively little new information provided to inform these issues which are of huge interest to investors, consumers and pensioners. What is profoundly clear however is that the implications for consumer choice, investors, pensioners and for all suppliers to the utility sector are very wide ranging and significant.

Nonetheless, taken together they mark a huge and unprecedented shift in the ownership and management of public services. They also mark moves designed to ‘future-proof’ the new ownership structures making them difficult to reverse by any future regime. For example, Labour’s proposals for energy include a “nested system that combines decentralisation and local national planning, and a fair allocation of costs.”

It is intended to allow decision-making at regional and local levels and involves setting up a National Energy Agency, Regional Energy Agencies, Municipal Energy Agencies and Local Energy Communities.

Labour acknowledge this will be a challenging structure to implement. But, if it succeeds in doing so, we believe the outcome would be that this system of national, regional and local structures would become so deeply rooted in local infrastructure and politics that it would become very hard to unwind in the future without engendering significant political and economic risk and enormous disruption.

Taken together, the plans to nationalise and to make it difficult to reverse in future create a key immediate question - will investors get paid compensation if the plans materialise and if so how much? As with other aspects of Labour’s nationalisation plans we believe we can provide some insight into considerations around compensation and will be happy to discuss those on further enquiry.

Hereafter a summary of Labour’s key policy proposals for the nationalisation agenda and wider policy around control of public services. The 2019 manifesto says:

- “We will put people and planet before profit by bringing our energy and water systems into democratic public ownership”.

- “In public hands, energy and water will be treated as rights rather than commodities, with any surplus reinvested or used to reduce bills. Communities themselves will decide, because utilities won’t be run from Whitehall but by service-users and workers.”

- “Public ownership will secure democratic control over nationally strategic infrastructure and provide collective stewardship for key natural resources.”

- “Whenever public money is invested in an energy generation project, the public sector will take a stake and return profits to the public.”

- “In the case of energy, it will also help deliver Labour’s ambitious emissions targets. Whereas private network companies have failed to upgrade the grid at the speed and scale needed, publicly owned networks will accelerate and co-ordinate investment to connect renewable and low-carbon energy while working with energy unions to support energy workers through the transition.”

- “Public services must also be accountable. Labour will end the current presumption in favour of outsourcing public services and introduce a presumption in favour of insourcing. And we will stop the public getting ripped off….”

However, despite trailing these policies for over 2 years, the Manifesto remains silent on key detail including:

- Priorities for nationalisation.

- Timings.

- Costs and how the programme will be funded.

- Compensation for, and treatment of, investors including treatment of both debt and equity.

- Impacts on UK pensioners.

- New models and structures including impact on current regulatory systems.

A key summary of nationalisation targets is set out below alongside brief highlights of other targets for taking back control over public services.

Energy

A new UK National Energy Agency will be established to own and maintain the national grid infrastructure and oversee the delivery of decarbonisation targets.

14 new Regional Energy Agencies will be established to replace the existing district network operators and hold statutory responsibility for decarbonising electricity and heat and reducing fuel poverty.

The Big Six energy companies (SSE, EDF Energy, British Gas, npower, E.ON UK and Scottish Power), who supply households, with energy will be bought into public ownership

Water

- Will be brought into public ownership, no further details

Broadband

- Establishment of British Broadband:

- Will contain two arms: British Digital Infrastructure (BDI) and British Broadband Service (BBS).

- This will bring the broadband-relevant parts of BT into public ownership with a jobs guarantee for all workers in existing broadband infrastructure and retail broadband work.

- BDI to be responsible for rolling out the remaining 90-92% of the full-fibre network and acquire necessary access rights to existing assets.

- BBS to be responsible for co-ordinating the delivery of free broadband.

- Funding to be achieved through taxation of multinationals and tech giants.

Royal Mail

- Royal Mail will return to public ownership at the earliest opportunity:

- It will be reunited with the Post Office creating a publicly owned Post Bank.

- This publicly owned Post Bank will run through the post office network to ensure every community has easy access to face-to-face, trusted and affordable banking network.

PFIs

- All (not some) PFI contracts are to be “taken back” over time.

- For services procured from the private sector, there will be an assessment against best practice in public service criteria – which include provisions for collective bargaining, fair wage clauses, adherence to environmental standards, effective equalities policies, full tax compliance and application of pay ratios (maximum of which will be 20:1).

Prisons

- PFI prisons are to return in-house and there will be no new private prisons.

- nProbation services will be reunified on a publicly run, locally accountable basis.

Land

- Land Registry (which has had several attempts at being privatised) is to remain in public hands and ownership of land is to be made more transparent.

- Public land for building low-cost housing will be bought through the establishment of a new English Sovereign Land Trust, with powers to buy land more cheaply.

- Brownfield sites are to become a priority for development.

NHS

- Labour plan to end and reverse NHS privatisation programmes:

- Repealing the Health and Social Care Act to reinstate the role of the Secretary of State to be responsible for providing the healthcare system.

- Health authorities will no longer be required to put services out to tender.

- Services will be delivered in-house and subsidiary companies will be brought back in-house.

- NHS land sales and assets will end.

- An infrastructure plan will return NHS England to the international average level of capital investment.

- A generic drug company is to be established:

- The Patent Acts provisions will be used to ensure fair prices for patented drugs along with compulsory licences and research exemptions to enable access to generic versions.

- All parts of the NHS (including treatment of patients, employment of staff and medicine pricing) are to be excluded and protected from any international trade deals.

- Labour will join up, integrate and co-ordinate care through public bodies to prevent further private sector delivery of health care.

Transport

- Bus networks will be regulated and taken under public ownership and resources and full legal powers will be granted to achieve this.

- Railways to revert to public ownership and options include franchise expiry:

- Publicly owned rail company will steer network planning and investments. It will co-ordinate mainline upgrades, re-signalling, rolling stock replacement and major projects and will implement a full programme of electrification (including in Wales).

- A long-term investment plan will include delivering Crossrail for the North, consulting to re-open branch lines, unlocking capacity and extending high-speed rail networks nationwide, completing HS2 and taking it to Scotland.

- Promotion of the use of rail freight and expanding the provision of publicly owned rail freight services.

- Taxi and private hire services licencing to be reformed.

Steel

- Establishment of a Foundation industries Sector Council to enable a clean and long-term future of steel.

- Support to the steel industry through public procurement, action on industrial energy prices, exempting new capital from business rates, investing in R&D and building three new recyclable steel plants.

Defence

- A Defence Industrial Strategy White Paper will be published and will include a national Shipbuilding Strategy for keeping all royal Navy and Royal Fleet auxiliary shipbuilding contracts in the UK.

The issues raised for: Suppliers to Government

Labour policy sets out a far-reaching agenda that broadly seeks to increase diversity and decrease income inequality. It proposes a novel but potentially powerful tool with which to achieve its desired outcomes - the proactive use of the UK Government’s £200bn annual procurement budget to further promote its ESG (environment, social and governance) goals and to ensure the “best standards on government contracts”.

The proposals will require any company tendering to Government (whether suppliers of widgets, infrastructure or asset management services) to be able to confirm it is compliant with a range of ESG factors to be considered for tenders including:

- paying own suppliers within 30 days

- paying taxes

- protecting the environment

- providing training

- reducing boardroom pay to meet a 20:1 pay gap

- recognising trade unions, and

- respecting equal rights of workers from day one of their employment.

If non-compliant then bidders (and we presume their own supply chains if part of the bidding offering) would be denied access to these business opportunities. We believe these proposals could be implemented quite quickly and are happy to discuss our understanding on further enquiry.

The issues raised for: Corporate Structure, Law and Employment

“Work should provide a decent life for all, guaranteeing not just dignity and respect in the workplace, but also the income and leisure time to allow for a fulfilling life outside it.” (Manifesto 2019)

There are ambitious and wide-ranging commitments to extend and codify worker rights, to help people balance work and family life, and to enhance trade union power.

Although the manifesto is light on detail, there is a clear vision to realign fundamentally the balance of power between workers, trade unions and employers.

The plans include additional protections for workers to tackle job insecurity and further family-friendly rights; increased state responsibility for maintaining minimum standards at work and for enforcing equal pay legislation. It will be easier for trade unions to organise, including a right for unions to access workplaces, collective bargaining rights to enable unions to negotiate minimum workers’ rights across a whole sector and less onerous rules on ballots. There are also radical ideas such as:

- A pilot of Universal Basic Income to respond to the challenges of low pay

- A ban on the dismissal of pregnant women without prior approval of a new inspectorate – the Workers’ Protection Agency

- A new Ministry for Employment Rights to “give working people a voice at the Cabinet table”

- One-third of boards to be reserved for elected worker-directors and give them more control over executive pay

- A new right for workers to a stake in the companies they work for (and a share in the profits they help create) by requiring large companies to set up Inclusive Ownership Funds (IOFs); up to 10% of a company will be owned collectively by employees, with dividend payments distributed equally among all, capped at £500 a year

Some old ideas have re-emerged such as employer liability for third party harassment and banning zero hours contracts, as well as new ones to enhance trade union rights to access workplaces to undertake sectoral collective bargaining. There are proposals to reduce the average full-time weekly working week to 32 hours, a living wage of at least £10 per hour for all works aged 16 or over, extending pay-gap reporting to BAME groups and new mandatory disability pay-gap reporting for companies with over 250 employees. There are also commitments to give all workers the right to flexible working and extra protection for pregnant women, those going through menopause and terminally ill workers.

There is a shift towards state (rather than individual) responsibility for upholding employment law protections and standards, including for enforcing equal pay legislation and ensuring employers take positive action to close the gender pay gap.

Overall - unsurprisingly - the focus remains heavily on extending and strengthening workers’ rights and security and equality at work. As a package, the proposals involve some significant practical considerations.

The issues raised for: Bilateral Investment Treaties

The Labour Party’s nationalisation proposals raise many questions including that of possible compensation for stakeholders.

There are broadly two avenues through which to arrive at a determination of any compensation: the European Convention on Human Rights (ECHR) and the provisions of any applicable bilateral investment treaty (BIT) with the UK. Interestingly two UK energy companies have recently announced their intention to use BITs: National Grid (proposing to use HK and Lux) and SSE (proposing to use Switzerland).

English law currently incorporates the ECHR as part of domestic law which provides a qualified right for compensation in the event of nationalisation. That provision rests on two conditions:

- the qualified right will not be breached if the nationalisation strikes a fair balance between public and private interests, and

- if the right were breached, the compensation that would be payable need only be reasonable in the context, which gives the State considerable latitude in assessing the compensation it is prepared to pay.

All of which said there is finally the theoretical possibility (at least) that any incoming Government could repeal the legislation incorporating the ECHR into English law leaving disgruntled investors only with the option of bringing claims before the European Court in Strasbourg, a forum with which the UK Government has previously had a somewhat laissez faire relationship.

An alternative to the ECHR route is to seek compensation under any applicable bilateral investment treaty (BIT) to which the UK is signatory. The UK has agreed nearly 100 BITs with foreign States which provide that investors from those foreign States into the UK are entitled to a number of protections in international law including:

- no expropriation without compensation, fair and equitable treatment and resolution of any disputes under the treaty applying international law before an international arbitration tribunal (our emphasis added).

If an investor into the UK has an investment treaty that meets the relevant standards then it could be entitled to full market value compensation for any investments nationalised by a new Government. We are happy to provide further details on BITs on further enquiry.

_11zon.jpg?crop=300,495&format=webply&auto=webp)

.jpg?crop=300,495&format=webply&auto=webp)

.jpg?crop=300,495&format=webply&auto=webp)

_11zon.jpg?crop=300,495&format=webply&auto=webp)

.jpg?crop=300,495&format=webply&auto=webp)

_11zon.jpg?crop=300,495&format=webply&auto=webp)

.jpg?crop=300,495&format=webply&auto=webp)