Among the private fund programs available for foreign asset managers who wish to explore and expand their business in China, the WFOE PFM programs and the QDLP/QDIE programs are among the most commonly used ones. Please see our recent write-ups here and here.

PFMs are for global asset managers to set up a PRC onshore fund primarily for capital raising within the PRC as well as making investments within the PRC, whereas QDLPs are for capital raising within the PRC while making investments overseas. It is recently understood from the Asset Management Association of China (AMAC), the de facto regulator of private funds in China authorized by China Securities Regulatory Commission (CSRC), and Shanghai financial services office (FSO) that AMAC and FSO are now ready to expand the business scope of WFOE PFM managers to allow them to launch overseas investment funds, effectively merging both the QDLP and PFM programs together.

Below are more details on these two programs and the implications following the combination of the two.

Regulatory background – the WFOE PFM program

Under the WFOE PFM program which was first introduced in 2016, a foreign asset manager is allowed to establish a wholly foreign owned enterprise or a joint venture in PRC which serves as a private fund manager entity. More than 30 foreign assets managers have established their onshore PFMs, and have launched more than 100 private funds under this program.

It is usually required for the direct foreign shareholders of the applicants to be financial institutions authorised or approved by recognised financial regulatory authorities of their home jurisdictions. Once duly registered with AMAC, the WFOE PFM manager is eligible to raise a private securities investment fund that invests in securities (a term narrowly referring to the more liquid securities in China) issued in China, including stocks, bonds, fund units and other securities and derivatives recognised by the CSRC.

As a general principle, the private securities investment funds launched by the WFOE PFM manager should not invest in securities issued outside of China, with the exception that they are allowed to trade Hong Kong stocks through the Stock Connect programs. Under such rules, investments into other overseas assets or funds were not feasible as such investments go far beyond the scope of the private funds launched by WFOE PFMs.

Regulatory background – the QDLP program

Qualified Domestic Limited Partnership (QDLP) or Qualified Domestic Investment Enterprise (QDIE) are pilot programs developed by the Chinese local governments, which allow foreign asset managers to raise RMB from institutional and high net worth investors in China for the purposes of overseas investments, through a Chinese feeder product.

The QDLP/QDIE programs are available in several cities/provinces such as Beijing, Shanghai, Tianjin, Shenzhen, the Greater Bay Area, Hainan, etc. There are 37 existing registered QDLP managers as of now, who have launched more than 40 QDLP funds.

Though the details of the QDLP/QDIE programs could vary from different locations, local authorities tend to adopt a similar regulatory framework:

- the QDLP program is quota-based, meaning the local program largely depends on the quota granted by SAFE;

- the local authority sets certain criteria for the applicant, such as a minimum capitalisation of the QDLP manager, necessary local investment management personnel, a licensed controlling shareholder, and minimum fund size of the QDLP fund, though certain pilot regions have relaxed some criteria in recent years;

- the process of establishing the QDLP manager and raising the QDLP fund require approval/confirmation by local government as well as necessary registration and filing with AMAC.

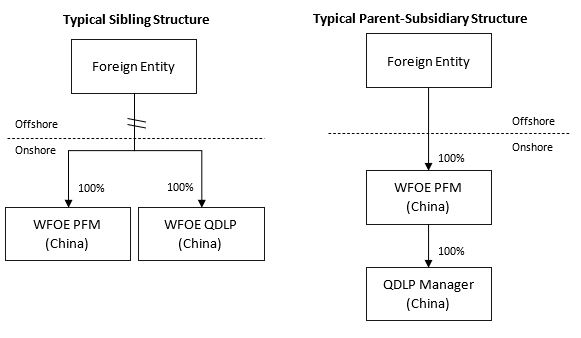

The evolving structure

Starting from 2017, in order to incentivise global asset managers to participate in both QDLP and WFOE PFM programs, the Shanghai government, among other relevant local governments, offered global asset managers the opportunity to synergise the QDLP and PFM practices by allowing: i) dual hatting arrangement of employees in a QDLP manager and a PFM manager; and ii) a QDLP manager and a PFM manager sharing the same address for the purposes of business and AMAC registration.

The incentives were proved to be effective, and it has led to a boost of new QDLP Managers being registered in 2018. Among foreign asset managers who have set up both a WFOE PFM entity and a QDLP entity, most of them have adopted the parent-subsidiary structure, while some adopt the sibling structure. One noticeable benefit of adopting the Parent-Subsidiary structure is that the capital contributed to the QDLP manager will be counted towards the capital requirements of the WFOE PFM manager, resulting in a more flexible capitalisation structure and allowing for 100% dual hatting between the employees of the two entities (which is not otherwise feasible under other structures).

Combination of QDLP and PFM

When they were first introduced to the market, WFOE PFM programs and the QDLP/QDIE programs had their own distinct objectives, and there were no overlaps in terms of their businesses. However, the market has been keen since 2021 when the Shanghai regulator revealed its plan to encourage an emerged and combined structure of the WFOE PFM and QDLP managers. Nevertheless, managers were somewhat conservative to adopt this structure at that time, as the structure had not yet been officially endorsed by CSRC and AMAC.

It is apparent that progress has been made this year, as the CSRC and AMAC have finally given the green light. Local authority such as the Shanghai government have been very active to promote this new policy and it is expected that an updated QDLP policy in Shanghai is under way.

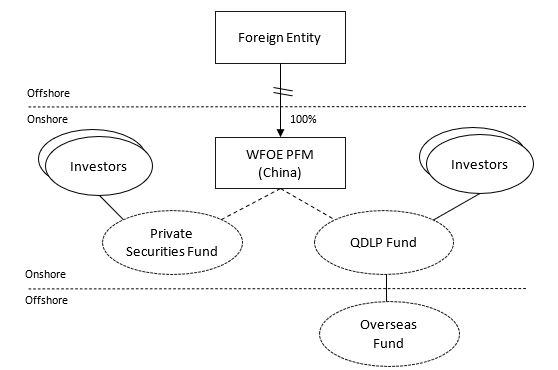

Under the new policies, a foreign asset manager who has an established WFOE PFM already in China no longer needs to go through the hassle of setting up a brand new corporate entity as a QDLP manager, which effectively enables the saving of costs spent in registering the QDLP as a manager with AMAC and operation and maintenance costs. Furthermore, WFOE PFMs are allowed to launch more diversified products with focuses on differentiated asset classes and strategies for PRC onshore and overseas markets respectively.

With the WFOE PFM being able to launch both domestic private securities funds and QDLP fund products, the new structure will provide a simplified and efficient solution for foreign asset managers who wish to explore both types of businesses, whereby the WFOE PFM structure can be utilised to minimise compliance and maintenance costs of the overall legal structure.

In China, close ended fund managers and open ended fund managers are regulated slightly differently and there is a general principle that a PE fund manager is not ought to launch an open ended fund and vice versa. After the combination of QDLP and PFM, it seems that PFM may be allowed to laugh QDLP funds that invest into overseas close ended funds whilst continuingly managing its onshore open ended funds. Hence it is generally believed that foreign asset managers with local WFOE PFMs are likely to achieve a higher synergy with its overseas affiliated managers in fundraising and investment activities carried out in the global market.

Please note that this article is produced by jointly Simmons & Simmons and Shanghai YaoWang Law Offices.

Should you have any questions or require further assistance regarding any of the above, please do not hesitate to contact us.

Melody Yang

Co-Head, Partner

Shanghai YaoWang Law Offices

T +86 21 8013 5022

M +86 135 2105 2486

melody.yang@yaowanglaw.com

_11zon.jpg?crop=300,495&format=webply&auto=webp)

_11zon.jpg?crop=300,495&format=webply&auto=webp)