HMRC re-evaluate their DeFi protocols

In February 2022, HMRC released new guidance on its view of the UK tax treatment of Decentralised Finance (DeFi) lending and staking activities.

Update: For details of the government’s proposal to review the tax treatment of DeFi lending transactions, see “UK review of cryptoasset regulation: tax aspects”.

To the surprise of the industry, HMRC has taken an indicative position that it considers most lending and staking activities will transfer 'beneficial' ownership in cryptoassets and therefore constitute disposal of an asset (with the accompanying tax consequences). In this article we discuss the principles of DeFi, HMRC's new guidance, and the response required when assessing any DeFi transactions undertaken.

What is DeFi?

DeFi has become a prominent feature of the crypto industry due to current (and potential) application in the lending and borrowing markets. DeFi offers financial services and products through utilising cryptography on public blockchains (primarily Ethereum) to trade, lend or borrow cryptoassets without reliance upon centralised third-party intermediaries such as brokerages, banks or exchanges. Instead, those seeking to trade, lend, stake or borrow cryptocurrency do so through the use of immutable smart contracts, programmed code stored on a blockchain that runs when predetermined conditions are met.

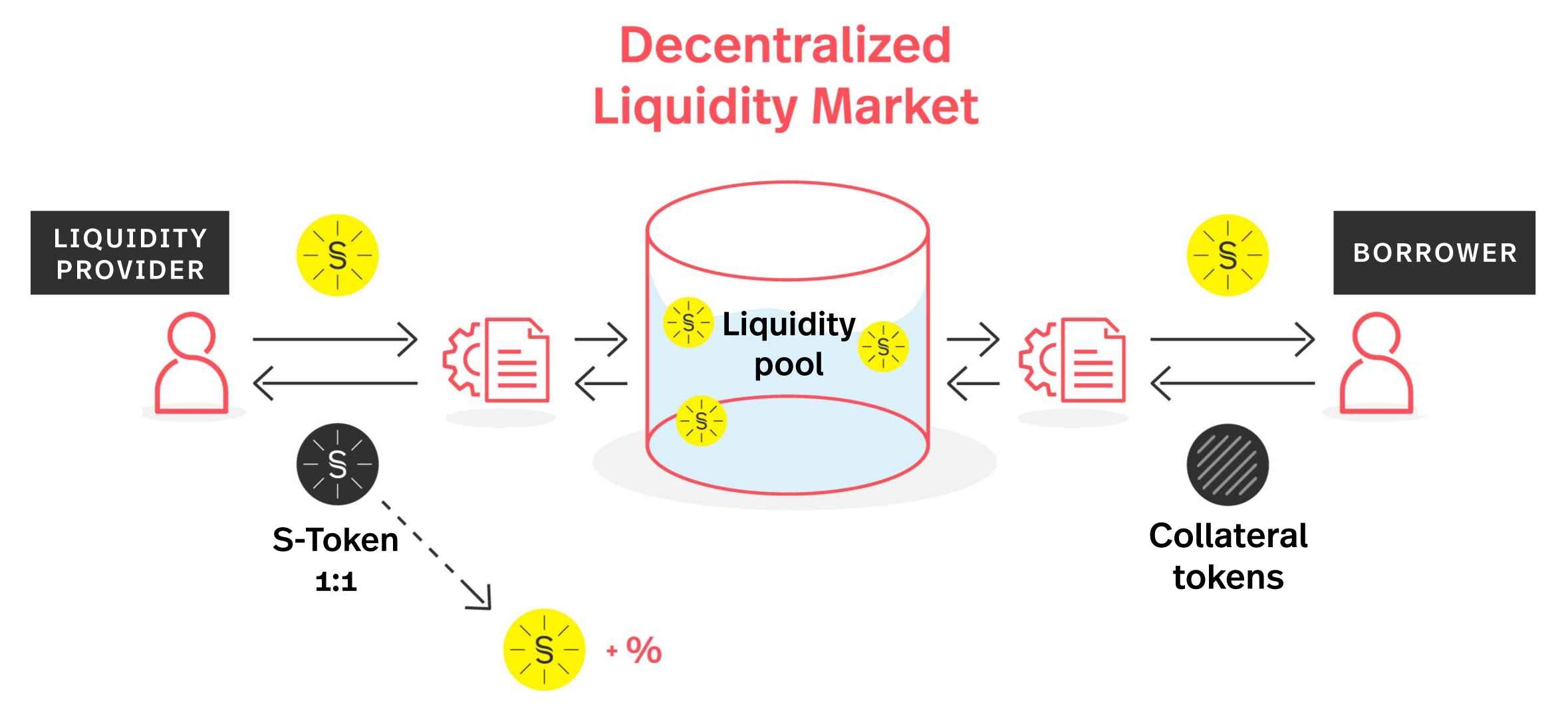

Initially, DeFi lending and borrowing was undertaken on a peer-to-peer basis with lenders and borrowers matched on decentralised marketplaces. Over time, inefficiencies in matching lenders and borrowers led to a shift to a peer-to-contract model through decentralised liquidity marketplaces (DLMs). Examples of these include AAVE or Compound, which operate on the Ethereum blockchain. Users can provide (or lend) cryptocurrency through 'staking' their tokens to the DLM liquidity pool in return for "interest" on their cryptocurrency. The lender is often referred to as a liquidity provider (LP). Borrowers are then able to borrow cryptocurrency from the liquidity pool, staking other cryptocurrency as collateral for the borrowed amounts (usually stablecoins such as USDC pegged to USD).

At a high level, DeFi lending and staking operates as follows (see diagram below):

- LP stakes their 'S-Coin' cryptocurrency to a DLM's liquidity pool through the operation of a smart contract.

- In return for the staked S-Coin, the LP automatically receives S-Tokens, which are representative of the deposited S-Coins in that they are redeemable 1:1 for the S-Coin provided (i.e., 1 S-Coin = 1 S-Token).

- By operation of the smart contract, the LP is entitled to recover its S-Coins (and any interest due) through the return of the S-Tokens at any time.

- The borrower's use of the DLM operates in much the same way but in reverse.

- The borrower stakes its collateral stablecoin in return for S-Coins.

- By operation of the smart contract the collateral is forfeited should certain conditions be met, for example if the price of the S-Coin drops to 80% of its value.

The increased use of DLMs can be attributed to the markedly higher rates of interest compared to traditional saving methods, driven by the demand for borrowing which is typically undertaken to exploit cryptomarket inefficiencies through arbitrage. These arbitrage opportunities can typically involve 'flash loans' which can typically take approximately 16 seconds to execute.

HMRC's new guidance on DeFi lending and staking

On 2 February 2022, HMRC released further guidance on the taxation of DeFi activities, focussing on the lending and borrowing of cryptoassets (CRYPTO60000).

The guidance explains that in most cases HMRC considers that staking and lending constitutes a disposal of an asset upon which tax would be due where there has been a gain. Specifically, HMRC has provided guidance and indicated that typical DeFi transactions would constitute two deemed disposals whether a party is acting as a lender/liquidity provider or a borrower:

In the case of the lender/liquidity provider, the first disposal is made on lending of tokens (or a deposit to a liquidity pool), and the second upon the return of any tokens received in receipt of the loan; and

In the case of a borrower, the first disposal is made through staking tokens as collateral for the loan and the second on the satisfaction of the principal borrowed (CRYPTO61650).

(Prior to publication of this guidance, many participants appear to have taken the view that lending/staking activities in DeFi, including acting as a liquidity provider or other staking, would not be treated as involving any disposal of the staked digital asset. In its earlier guidance, HMRC had instead placed much of its emphasis on the taxation of returns from DeFi activities rather than on the initial stake. However, HMRC now opine that "the making of a DeFi loan/staking may give rise to a disposal of a chargeable asset" (CRYPTO61600).)

Applying this to the worked example above, the LP would be deemed to have made a disposal once they provided the S-Coin to the liquidity pool (CRYPTO61620). Accordingly, it is likely that on redemption of the S-Coin, HMRC would treat the S-Token as its own cryptoasset which is disposed of together with a reacquisition of the S-Coin. To the extent amounts received as "interest" arise, this income may be excluded in any gain computation. However, this determination would need to be made on a case-by-case basis and of course, adds further complexity.

Further, HMRC added that it does not consider most cryptoassets to be securities for the purposes of the 'repo' regime (under sections 263A or 263B TCGA 1992) which applies to the sale and repurchase of securities such as company shares (CRYPTO61610). While some crypto lending/borrowing or DeFi type transactions may share characteristics with stock lending, it does not in HMRC's view benefit from the same tax treatment.

There has been an increased presence of hedge funds, asset managers, financial institutions and HNWI in the DeFi space, and if they have taken the position that a disposal is unlikely to have been made, the tax consequences for them as taxpayers could be significant (however this is also dependent on the particular profile of the taxpayer). If the entirety of a taxpayer's DeFi related transactions would be deemed disposals, each transaction will need to be retroactively assessed to evaluate the price of the relevant cryptoassets and the consideration treated as given for their disposal at the point of lending/staking and at the time when any loan/staking transaction is satisfied. This is required to assess whether tax is due on a gain made from the initial value when the relevant cryptocurrency was acquired. Plainly this could be administratively burdensome, especially if a flash loan related strategy was implemented. This compliance and accountancy burden is further exacerbated by the inherent volatility that is present in the cryptocurrency market where average 5-10% price changes can occur on a daily basis (with some intraday volatility on cryptocurrency being considerably higher).

Notwithstanding the administrative burden, upon completion of an internal assessment, taxpayers may also be caught out by an unexpected tax bill for gains made and unable to offset these against capital losses (which can only be used against capital gains arising in the same period or carried forward but not carried backward).

The legal complexities in determining disposals

HMRC has provided worked examples on a host of different staking and lending activities and in each case has reached the conclusion that a disposal is likely to have taken place upon the lending or staking of the cryptocurrency.1

However, there may be instances where a disposal has not taken place. As HMRC's guidance recognises, whether a disposal has been made will turn on whether 'beneficial ownership' has been transferred (CRYPTO61620). Whilst the English courts have generally reached a consensus that cryptoassets are property (rather than money), the question as to what the nature of ownership is still remains to be answered, including whether cryptoassets are a 'chose in action', a 'chose in possession' or another form of personal property.2 The importance of this determination has a direct correlation as to whether there is retention of a 'beneficial' right in cryptocurrency.

DeFi is a thoroughly modern concept, but it will be taxed in accordance with rather old principles of the law of personal property, which generally treats pooling of identical assets as the extinguishing of proprietary rights. The law in this area is complex and cases turn on fine factual points.

Seeking to apply the common law in order to prove that a disposal has not taken place will therefore require an in-depth factual investigation and analysis into the intricacies of the DeFi transactions taking place, including the following items:

- The type of cryptoassets;

- the operation of the DLM platform;

- the operation of the smart contracts including how the asset is transferred;

- the underlying blockchain protocol;

- the nature and fungibility of the coins deposited and of the token in receipt; and

- in what form the deposited coin is returned (for example, whether the coin returned is represented by new data).

Each type of DeFi transaction will have nuances which means each will need to be assessed in its own right. Ultimately the burden is on the taxpayer to analyse their usage of individual DeFi platforms and protocols to demonstrate to HMRC that each time the taxpayer has lent or staked, or where a transaction was satisfied, they were not in fact making a disposal. This will be particularly tricky for taxpayers who have operated a range of DeFi strategies in their trading activities across a number of platforms and protocols.

Challenging HMRC on Staking Activities

By taking the view that all manner of DeFi activities will constitute disposals, HMRC has thrown down the gauntlet to taxpayers. HMRC is clearly very alert to the opportunities for potential recovery of tax in this space and may very well have their crosshairs in particular on financial institutions, asset managers, funds and HNWIs who are operating in this space. HMRC have already sent nudge letters to taxpayers and issued data holder information notices to crypto-exchanges, to take a view on any tax due in respect of crypto related activities. That coupled with the position HMRC has now taken may be the opening salvo in further investigation.

Unfortunately for the taxpayer, the onus is upon them to persuade HMRC that whilst lending and staking activities have taken place, a disposal has not occurred. Considering the extent of the penalty powers HMRC has, it is therefore important that any investigation into DeFi transactions is undertaken promptly, and an analysis reached as soon as possible. It would therefore be prudent for taxpayers to be proactive not only in their review of whether additional tax may be due on transactions but also whether any necessary engagement with HMRC is required to settle amounts due and to avoid further penalties. Where future transactions are due to take place then a risk-based approach should be considered by the taxpayer as to whether it follows HMRC's guidance or instead makes a disclosure to HMRC that it has departed from it (including through consideration of the factors mentioned above), with an expectation that an enquiry will follow. The usual health warnings about conducting effective, privileged investigations will apply.

Taxpayers subject to good compliance practices would require the production of tax advice to assess the above risks prior to entering into DeFi related transactions. Any advice given should provide an assessment of tax risks and include sufficient analysis taking a view on whether the staking would constitute a disposal, and the risk that HMRC would not accept such an analysis.

Recourse for bad tax advice

If upon review it is found that adequate tax advice has not been provided and a taxpayer faces an assessment and penalty from HMRC, there may be parallel recourse against the advisor in professional negligence. However, there will be a number of factors to take into consideration including HMRC's unexpected policy in this area and whether HMRC has been sufficiently tested on its position in the courts.

Nevertheless, when considering recourse against an advisor, any factors affecting limitation (including the terms of engagement letters) should be borne in mind. This is particularly important when HMRC are conducting an investigation in parallel. HMRC investigations can operate for a number of years and by the time an assessment by HMRC is given, the limitation period for any claim against an advisor may have expired. Therefore, it is important that any potential professional negligence claim against an advisor is at the forefront of a taxpayer's mind when assessing the matters discussed above. (For that reason, specialist advice should be sought.)

1 HMRC has already released an update to one of its examples which shows that even fundamental DeFi transactions are not so straightforward.

2 See Legal Statement on Cryptoassets and Smart Contracts UK Jurisdiction Taskforce, November 2019

.jpg?crop=300,495&format=webply&auto=webp)

.jpg?crop=300,495&format=webply&auto=webp)

_11zon.jpg?crop=300,495&format=webply&auto=webp)

.jpg?crop=300,495&format=webply&auto=webp)

_11zon.jpg?crop=300,495&format=webply&auto=webp)

.jpg?crop=300,495&format=webply&auto=webp)

.jpg?crop=300,495&format=webply&auto=webp)