Amendments to remuneration rules for dual-regulated firms

The FCA has published its draft proposals for the changes to SYSC 19D applicable to banks and credit institutions under CRD 5.

On 3 August 2020 the FCA published its consultation paper on Updating the Remuneration Code for dual-regulated firms, SYSC 19D, (the Code) to reflect the remuneration changes being implemented under CRD 5 (CP20/14). The changes are needed to allow the UK to transpose the remuneration aspects of CRD 5 by the 28 December 2020 deadline (which is required under the terms of the EU Withdrawal Agreement).

Summary of key changes

Timing. The FCA has proposed that firms apply the amended remuneration requirements from the next performance year beginning on or after 29 December 2020. The consultation period closes on 30 September 2020, meaning that firms with a 31 December performance year end would have a period of 3 months to finalise the changes to their remuneration arrangements in order to comply.

Proportionality. The FCA proposes to increase the proportionality threshold from €5bn to €15bn for firms that have:

- no obligations, or are subject to simplified obligations, for recovery and resolution planning purposes;

- a small trading book, ie traded business ≤ 5% total assets and < €50m;

- traded derivatives positions ≤ 2% of total on- and off-balance sheet assets; and

- overall derivatives positions of a total value of ≤ 5%.

The FCA says that it would like to preserve the current proportionality threshold so far as possible and prevent additional complexity and cost for firms in scope. Further, a €15bn threshold better reflects the nature and size of dual-regulated firms in the context of the UK market. Note the FCA’s proposals on converting the CRD 5 financial thresholds form Euros to Sterling (discussed further below). Based on the FCA’s current proposals, the Sterling equivalents of the proportionality thresholds in CRD 5 would be £4bn (€5bn) and £13bn (€15bn).

Interplay with Investment Firms Prudential Regime. The FCA confirms that solo regulated investment firms subject to the new Investment Firms Prudential Regime (the IFPR) will not need to apply CRD 5/CRR 2 requirements for the period between 29 December 2020 and the implementation of the IFPR in summer 2021. This will be a welcome relief for UK investment firms currently subject to CRD 4/CRR.

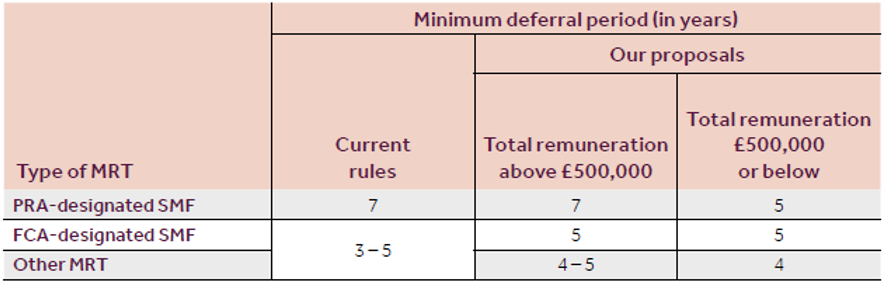

Deferral. This is to remain at 7 years for Material Risk Takers (MRTs) who perform a PRA-designated senior management function (SMF). However, the FCA recognises that the (significant) lowering of the individual de minimis threshold currently used to exempt MRTs from the Pay-out Process Rules will mean that a larger number MRTs will be subject to deferral. Accordingly, the FCA proposes to set different minimum deferral periods for those individuals whose total remuneration is below £500,000, namely the minimum deferral periods required by CRD 5 (four or five years).

The FCA also proposes to introduce FCA-designated SMFs as a separate category of MRTs for deferral purposes. The new category would be relevant to individuals with total remuneration both above and below £500,000.

The table below demonstrates how the deferral periods would change under the new Code:

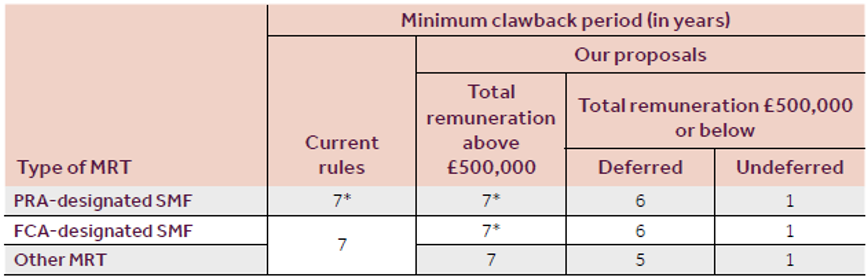

Clawback. Clawback periods will also change. Under the new rules, MRTs who receive total remuneration of £500,000 or more will continue to be subject to a 7 year deferral period. MRTs with total remuneration of up to £500,000 will be subject to a clawback period of that equal to the sum of the minimum deferral and retention periods under CRD 5. Firms will be permitted, in certain circumstances, to extend the clawback period to 10 years for MRTs performing PRA- and FCA-designated SMFs.

The table below demonstrates the new clawback periods under the Code:

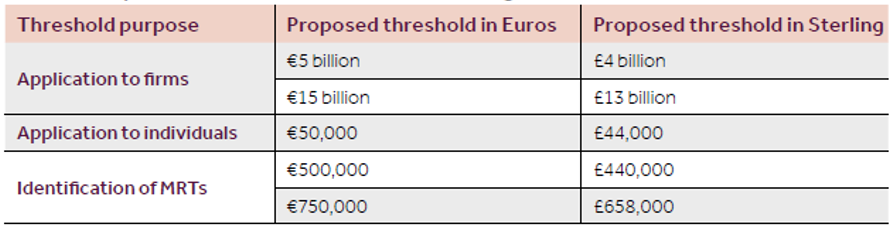

Euro to Sterling conversion thresholds. The FCA intends to convert the proportionality thresholds in CRD 5 from Euros to Sterling from 1 January 2021, including those applicable to the identification of MRTs under the quantitative criteria in the EBA’s revised RTS. These Sterling thresholds will mirror those the PRA proposes to set in its consultation paper on CRD 5 (CP12/20), published at the end of July.

The table below shows the FCA's proposed conversions into Sterling:

Next steps

The consultation closes on 30 September 2020. All dual-regulated firms impacted by the changes should have now started amending their remuneration arrangements in earnest to prepare for them. This is especially the case for firms with a 31 December performance year end.

.jpg?crop=300,495&format=webply&auto=webp)

.jpg?crop=300,495&format=webply&auto=webp)