On 16 January 2020. the FCA issued a number of papers, in conjunction with the Bank of England and the Working Group on Sterling Risk-Free Reference Rates (RFRWG), which reaffirm the objective of LIBOR ceasing at the end of 2021 and tour the horizon of what regulators expect to see firms achieving on an orderly transition to SONIA in 2020.

What is clear is that is that 2020 will be a key year for transition and firms are expected to accelerate their efforts.

The joint announcement is available here.

The key points coming out of the suite of documents are as follows:

1. Regulatory expectations and key dates in 2020:

In 2020, the FCA expects Senior Managers to focus on:

- ceasing issuance of cash products linked to GBP LIBOR by end-Q3 2020

(RFRWG roadmap available here) - changing the market convention for the GBP interest rates swaps

market to SONIA from 2 March 2020 (announcement is available here); and - significantly reducing the stock of LIBOR referencing contracts by Q1

2021.

There is now a clear cut-off date (end of Q3 2020) beyond which regulators consider firms should no longer be issuing cash products linked to Sterling LIBOR (if they will mature after the end of 2021). Action should be taken now given that many transactions may take months to complete and where it is possible that a planned IBOR-linked issuance may in fact launch after end of Q3 2020, relevant parties should consider whether it is necessary to apply an alternative reference rate.

In terms of ongoing regulatory engagement, in the joint letter sent to Senior Managers of major banks and insurers (available here), the FCA and PRA state that they will step up engagement with firms on LIBOR transition through the following channels: regular supervisory relationship, review of management information and by collecting data from firms (including data which some dual-regulated firms were required to provide by 31 December 2019). The letter also suggests that FCA contemplates that additional prudential tools (unspecified) may be applied to achieve the above objectives.

For Q1 2020, the FCA considers that action in the following areas is key to delivery, and should feature in firms’ planning from Q1 2020:

product development;

reviewing infrastructure, including updating loan system capabilities;

client communications and awareness; and

updating documentation.

2. Establishing a remediation framework for legacy contracts (including tough contracts):

Firms are strongly encouraged to focus on remediation strategies with a view to significantly reducing the stock of Sterling LIBOR linked contracts by Q1 2021. There is an acknowledgement that certain contracts will be challenging to remediate.

In this regard firms are expected to encounter various practical challenges in remediating certain products, in particular those for which consents may be required from third parties and/or securityholders. Firms should therefore take action promptly to complete due diligence and remediation planning and formulate remediation strategies for challenging products.

3. SONIA term rates:

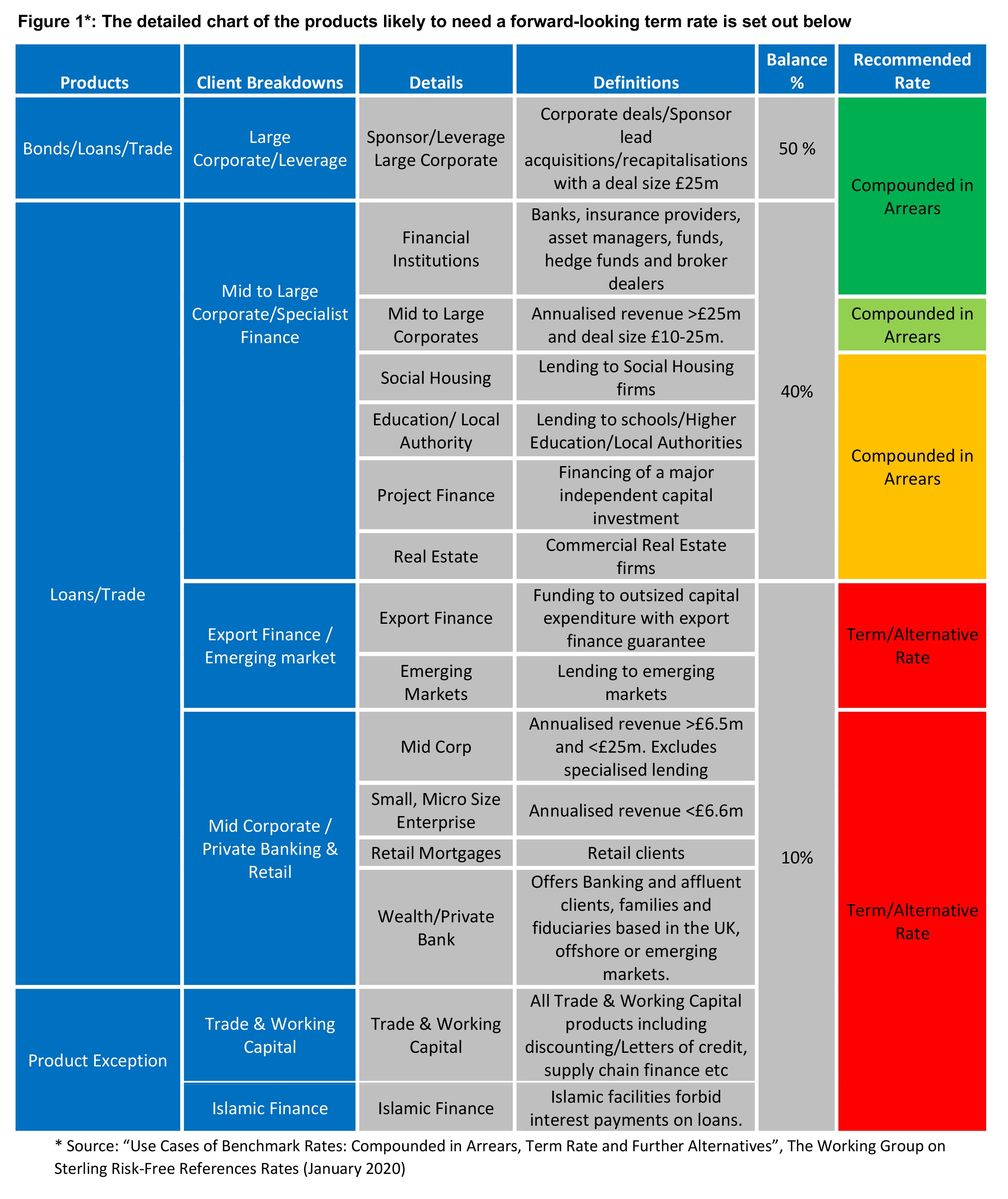

The RFRWG has consulted on the term SONIA reference rates (TSRR) (Use Cases of Benchmark Rates: Compounded in Arrears, Term Rate and Further Alternatives available here).

The prevailing view of the RFRWG is that SONIA, compounded in arrears, will be suitable for use and should be preferred for the majority of instruments. However, importantly there is a material concession that for 10% (by value) of the GBP LIBOR market, compounded in arrears is not suitable and certain sectors will require either forward looking term rates or alternatives (for example a fixed rate or overnight Bank Rate may be preferred). The sectors identified are: export finance, emerging markets, mid-corporate, private banking and retail, trade working capital and Islamic finance.

This is a significant shift in the emphasis from UK regulators away from compounded in arrears and forms the new blue print for what transition will look like. See Figure 1 below for more detail on products likely to need a forward-looking term rate.

The effort to develop effective SONIA term rates is being stepped up. Before Q2 2020, four administrators are expected to publish an initial ‘beta’ TSSR to be used for testing purposes. In Q3 2020, a provisional live SONIA Term Rate will be published to support those market participants that require alternative rates.

We would expect, in line with the RFRWG’s findings, that the majority of capital markets instruments which reference SONIA will reference SONIA compounded in arrears rather than a TSRR. The loan market (especially for SMEs) is acknowledged to be one of the primary markets that will benefit from a TSRR.

The wait for TSRR to develop will significantly impact firms’ transition plans and invites further delays to the start of repapering for the affected sectors of the market. Furthermore:

While the FCA estimates that only 10% of the market by value will be

affected, the clients affected by this change are principally SME and

retail. Therefore, the proportion of counterparties by number can be

much higher for some financial institutions which may now be put in

to a holding pattern until the TSRR market conventions settle down.The bifurcation of the GBP market between Compounded Overnight in

Arrears (CORIA) and TSRR as envisaged by the FCA raises questions

around: (a) if 90% of the market funds itself on CORIA: the stability

and liquidity of TSRR for the 10%, (b) whether the FCA’s preference

to introduce CORIA for the corporate sectors is now in jeopardy if

unregulated clients conclude that there is a choice, and (c) what

implications the FCA’s move has for transition and the programme to

develop forward-looking term rates in the USD, EUR, CHF and JPY

markets.Changing to TSRR will make the amendments to legacy business much

simpler on paper; but no industry consultation is currently in place

to agree the basis of the spread adjustments that are appropriate to

TSRR. The current LMA consultation looks at this question in relation

to cessation and pre-cessation fallbacks only. Retail and SME are

where the litigation risks of transition are concentrated: does the

situation invite the industry to undertake a cost/benefit analysis of

foregoing the spread adjustment for the SME and retail clients that

make up the 10%?

4. Adjustment spreads:

Very little is said on this key subject. The FCA’s Consultation from December 2019 (available here) closes 6 February 2020 but only focusses on setting adjustments for cessation and pre-cessation fallbacks.

In particular, the Consultation does not address methodologies suitable for voluntary transition to SONIA prior to cessation or adjustment spreads for forward looking term rates. Further work on this topic is clearly required, especially in view of the acknowledgement from the RFRWG and FCA that certain contracts require term rates. The methodologies in scope of the FCA Consultation include:

ISDA historic median approach: credit spread adjustment based on

different between GBP LIBOR and SONIA-derived rate calculated using a

median over a 5-year lookback.ISDA forward approach: calculated based on observed market prices for

the forward spread between GBP LIBOR and the SONIA-derived rate. A

forward spread curve up to 30-60 years for the SONIA-derived rate in

each relevant tenor would need to be published on a daily basis until

the cessation of GBP LIBOR.ISDA spot- spread approach: based on the spot-spread between GBP

LIBOR and the SONIA-derived rate on the day preceding the fallback

trigger date. This is similar to the historical median approach and

derives a single value for the credit adjustment spread, but

references a very short period.

5. Establishment of three new Working Groups:

The RFRWG is launching three new working groups focussing on:

- enablers to moving new loans issuance away from GBP LIBOR;

- frameworks to support transition of legacy cash products; and

- providing market input regarding the ‘tough legacy’ of products that

may prove unable to be converted or amended to include robust

fallbacks.

6. Bond market consent solicitation:

The RFRWG has acknowledged the challenge of remediating legacy capital markets issuances and encouraged the use of consent solicitation where securityholder consent is required to transition to SONIA. (Progress on the Transition of LIBOR – Referencing Legacy Bonds to SONIA by way of Consent Solicitation, RFRWG (January 2020) – available here)

The Cash Market Legacy Transition Task Force has been established to facilitate transition and has published six points for consideration in relation to the consent solicitation process. Among these the RFRWG notes that consent solicitations undertaken to date have not typically involved the payment of consent fees, which seems to suggest that this position is expected to be the norm.

The RFRWG also emphasises the importance of careful review of contractual documentation to ensure that consent solicitations observe associated requirements such as in relation to timing and sequencing. Issuers and product manufacturers will be aware of the practical challenges of implementing changes to securities through the consent solicitation process. In view of these challenges, issuers and product manufacturers should identify products which may require modification through a consent solicitation process and plan a timely remediation strategy (including an analysis of the position where the consent solicitation process does not give approval for rate transition).

7. Loan markets and SONIA uptake:

In 2019, the market began issuing SONIA linked loans, 3 originations occurred with 1 conversion of a LIBOR linked loan to SONIA. However, the loan market is adapting more gradually than derivatives market due to barriers to use. The RFRWG has identified the following developments which should aid uptake:

- IT systems at loan providers are being developed to allow for

widespread usage of SONIA - Treasury management systems at corporates are being similarly updated

- LMA and participants are developing standardised documentation

- Market conventions are being established for calculation of interest

in SONIA references loans

.jpg?crop=300,495&format=webply&auto=webp)

.jpg?crop=300,495&format=webply&auto=webp)

_11zon.jpg?crop=300,495&format=webply&auto=webp)

_11zon.jpg?crop=300,495&format=webply&auto=webp)

_11zon.jpg?crop=300,495&format=webply&auto=webp)